Round #48: NBA Trophy-Backed Financing... Sorta

Central Bank Rates; MSG Debt Restructuring; SRT Growth; Apollo's 2 Cents; BDC Dividend Coverage; Notable Deals; Bulletin Board

In Round #48:

Recent central bank rate decisions

A plot twist in last year's MSG Networks debt restructuring

Blackstone's SRT push and market growth

Reminding Apollo of its BDC's recent past

Non-fatal BDC dividend coverage shortfall

Notable Q2 deals

Bulletin Board

Disclaimer: there are 4,200+ of us here discussing private credit and leveraged loans, which is not a big world. At some point, I will probably throw punches at your company. I am blunt and sarcastic and, as friends like to remind me, too mouthy to live to an old age, so my take likely won’t please you. But don’t worry, next week it will be someone else in the spotlight and you will quietly nod along in satisfaction.

Also, none of this is investment advice.

1. Rate Rage

Mystic circumstances conspired to prevent me from writing a letter this week, but my relentless urge to rant about credit prevailed... albeit with a slight delay.

As you recover from that opening monologue, let's revisit the latest central banks rates.

Bank of Japan

The BOJ raised its policy rate by 0.25% to the highest level in 31 years... all the way to 1.0%! It was in response to Middle East-related inflation pressures, yet inflation is still running at just 1.4%. I mean, can we all just move there?!

European Central Bank

ECB wasn't about to be outdone either and hiked rates by the same 0.25%, marking its first hike since 2023, also citing Middle East developments. They expect inflation in the eurozone to average 3% this year before cooling to 2.3% in 2027 and 2.0% in 2028.

The Federal Reserve

The Fed, under its new chairman, Kevin Warsh, wasn't peer-pressured into hiking and kept rates unchanged at 3.50%-3.75%. But that might not last, as policymakers were split between keeping rates unchanged for the remainder of the year and delivering one or more quarter-point rate increases. Same reason... inflation driven by the war with Iran.

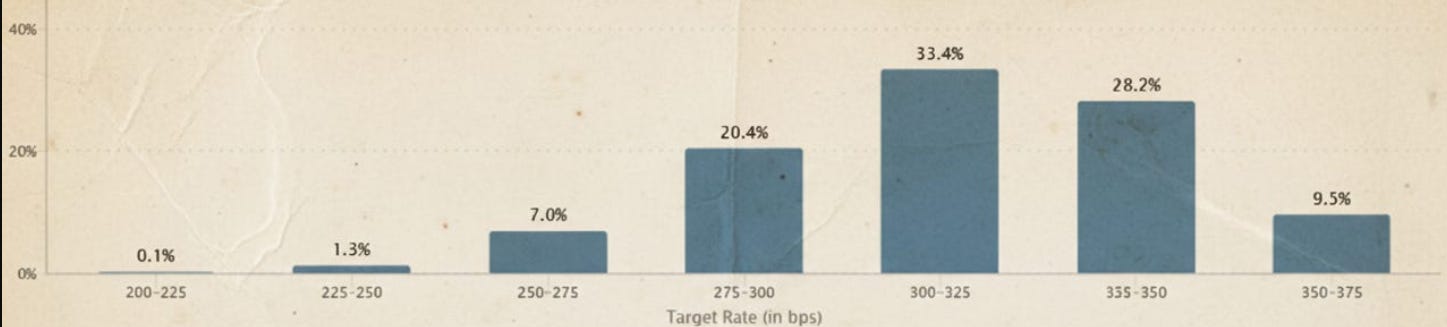

The chart below is from February 3rd, when only 9.5% of experts thought rates would stay flat for the year, and most market participants were debating whether there would be one, two, or even three rate cuts this year. Those were the days, huh?

Now, my only question is...

2. NBA Trophy-Backed Financing…Sorta

NBA fans (except perhaps those in San Antonio) would be intrigued by Bloomberg’s article New York Knicks’ Success Is a Win for Lenders Who Propped Up Broadcaster.

The article opens with this paragraph:

Just a year before the New York Knicks earned a spot in the NBA Finals, the company that broadcasts its games was thrown a lifeline to avoid a potential bankruptcy filing. Now, the lenders who backed that restructuring are likely cheering on the team’s success.

This makes little sense, so let me give some background.

This thing below is Sphere, the main property of Sphere Entertainment Co. (SPHR), a publicly traded company.

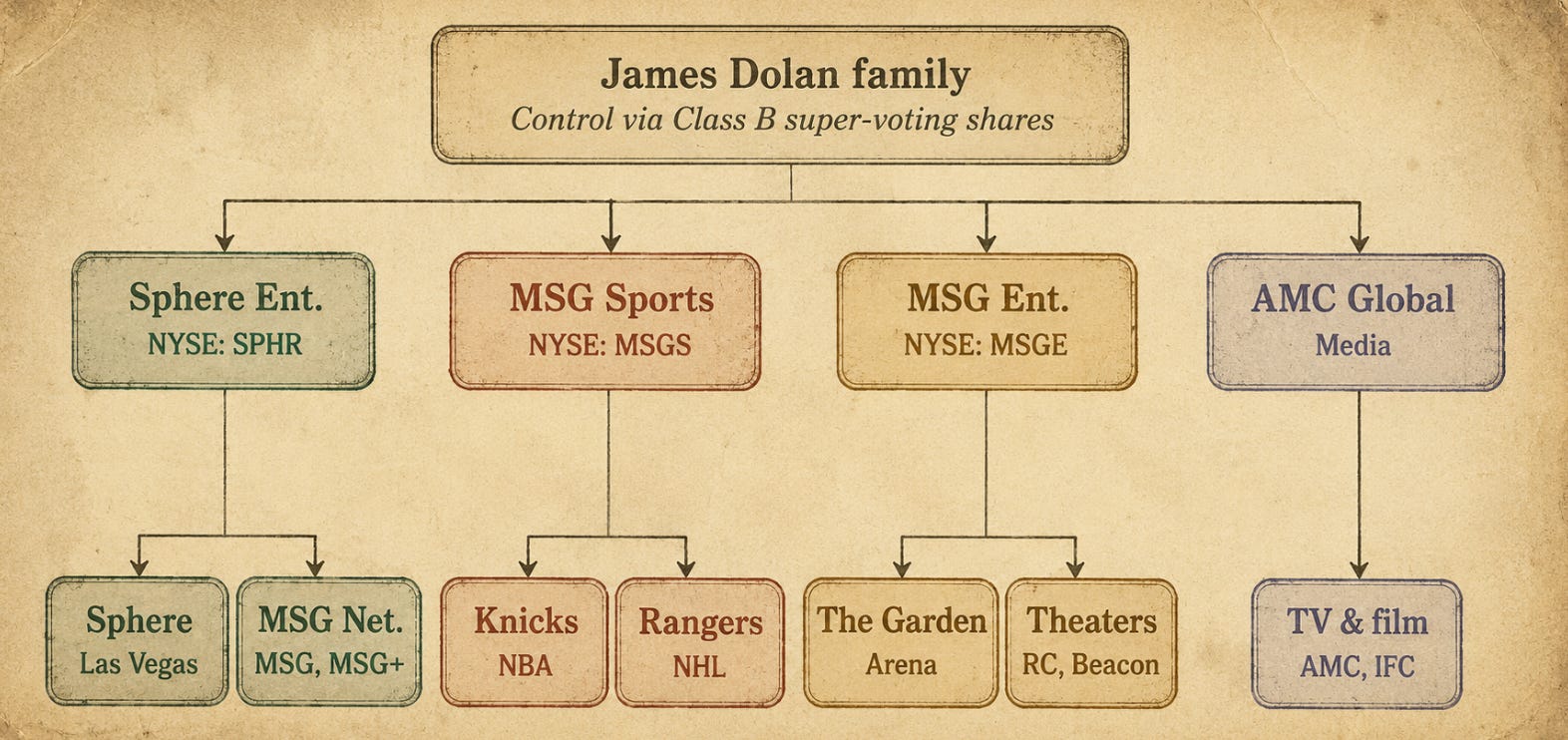

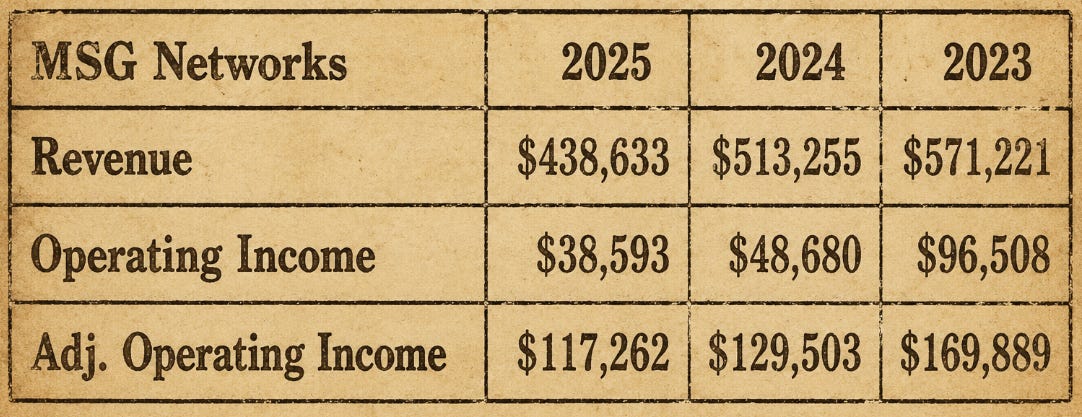

SPHR also owns MSG Networks, which operates New York regional sports channels as well as the subscription-based streaming service MSG+. The main programming on these channels largely consists of broadcasts of New York Knicks (NBA) and New York Rangers (NHL) games, along with other content related to these two franchises. That may sound a little strange until you realize that MSG Networks and the sports franchises are controlled by the same person, James Dolan, whose family owns a minority stake but retains majority voting control. See the chart below, but keep in mind that we will be discussing only the left half of it.

So, back in October 2019, MSG Networks got a 5-year, $1.1B term loan from a group of lenders led by JPMorgan, priced at LIBOR+1.25% to 2.25% depending on leverage (LIBOR has since gone away). Keep in mind, even though MSG Networks is a subsidiary of publicly traded SPHR, the parent didn’t guarantee the debt, so it isn’t on the hook for it. MSG Networks’ financial information is available in SPHR’s SEC filings, but because the company went through multiple restructurings, you can’t really get the figures going back to 2019. You can get the past three years of financials, though.

I’m sure the 2019 figures looked better than what we’ve seen over the past three years because, as you can tell, things haven’t exactly been moving in the right direction. Not only has the top line been declining, but that gap between Operating Income and Adjusted Operating Income is largely driven by restructuring charges. Also, see that significant drop in revenue over the past year? It was due to the sale of certain assets to Altice, which is so random, I swear Patrick Drahi (see last Round) is following me around.

Alright, 5 years into the loan, it nicely amortized to $830m, and was supposed to be paid off by October 2024… which didn’t happen. See, that “Operating income” is a much better proxy of the amount of cash the company generates than its “Adjusted” alter ego, so clearly they had a hard time accumulating $800m+. The failure to pay the debt triggered an event of default, which allowed lenders to demand immediate repayment of the loan. In this instance, though, that right didn’t mean much because the company clearly couldn’t repay the debt. In other words, lenders could have taken the keys. Instead, after some negotiations, they entered into a forbearance agreement.

In case you are not familiar, when borrowers breach covenants, they usually go back to the lenders, agree to a revised covenant package, pay fees, and amend the credit agreement to waive the default caused by the breach. That’s pretty common. The only people who tend to complain about it are clueless media outlets and distressed debt funds that were hoping to step into the situation, but now can’t because the lender and borrower decided to work it out. The alternative is a forbearance agreement, which usually comes with its own guardrails, often including new covenants, but does not waive the default. It’s basically a temporary truce that says, “You can keep operating, but we still haven’t forgotten that you owe us the money or the keys.”

Alright, during the forbearance period, MSG Networks continued paying interest and loan amortization, so by the time the permanent solution was implemented in July 2025, there was about $800m still outstanding. As part of the solution, MSG-related entities (including SPHR) made an $80m payment to the lenders, reducing the debt to $720m. In return, the lenders cut the debt to $210m (!!!), resulting in more than a $500m debt reduction, extended the maturity to December 2029, and significantly increased the price to SOFR + 5.00% (from LIBOR + 1.25% to 2.25%). In addition, the loan was to be amortized by $10m per quarter, plus the lenders were entitled to a quarterly excess cash sweep above a certain minimum cash balance. That last piece really accelerated the repayment because between July 2025 and December 2025, the loan balance declined from $210m to $159m.

But that is not even the most interesting part of the deal yet. As part of this amendment, the lenders got special rights that work like this: after the term loan is fully repaid, the lenders can continue sweeping 50% of excess cash flow through the earlier of (i) December 31, 2029, or (ii) until they have received $100m in cumulative payments. In other words, when that outstanding $720m was reduced to $210m, there was also an additional $100m of potential upside for the lenders.

Now, the rest of Bloomberg’s article will make more sense:

The Knicks’ playoff run is a potential boon for MSG Networks, part of Sphere Entertainment. The nationally televised Finals won’t give it any direct revenue, but the team’s winning ways could drive cable and streaming subscriptions from a large, die-hard fanbase that hasn’t experienced a championship win in more than 50 years.

“While MSG Networks won’t directly benefit from the Knicks lengthy 2026 playoff run, the local network could see ratings benefit next season from the solid playing momentum and team star power,” said Kevin Near, a Bloomberg Intelligence analyst.

One question you might be asking yourself is: why didn’t the lenders take the keys instead of writing off $400m-$500m of debt? Aside from the fact that few lenders want to run underperforming companies, imagine owning MSG Networks, knowing that James Dolan still controls the Knicks and Rangers, without which the network is pretty much worthless. It’s like confiscating someone’s car but having to ask them for the keys every time you want to drive it. Good luck with that.

3. SRTification Trend

In last week’s piece, Bloomberg covered Blackstone’s aggressive push into the Significant Risk Transfer (SRT) market, which it finds particularly attractive, and its plans to work with banks in Europe, Asia, and the Middle East.

The quote below is at the heart of the article:

SRTs allow banks to free up capital for more profitable business. The instruments appeal to investors because they typically offer returns exceeding 10% in exchange for insuring a junior risk on a loan portfolio. Large asset managers, such as Blackstone, have almost quadrupled the amount of capital deployed to SRTs since 2022.

“We’re doing more with banks than ever before in the history of our credit business by far,” Dan Leiter [Blackstone] said.

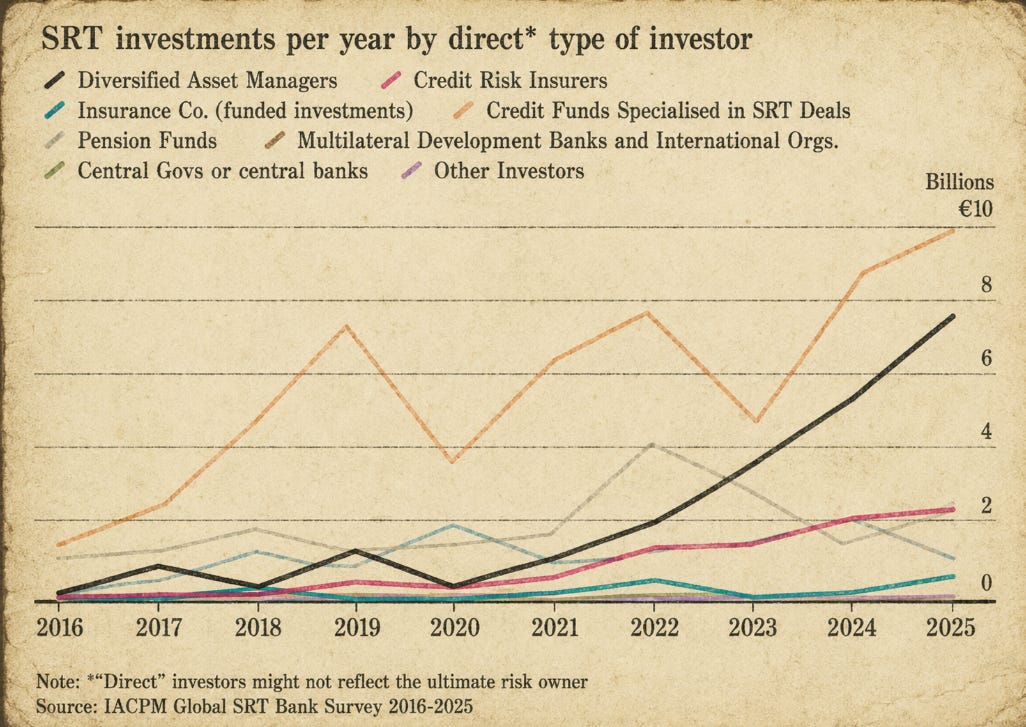

I broke down SRTs several months ago in Round #14: SRTonin: Happy Hormone of Risk Transfer, and I’m glad I did. Not only has the market for SRTs grown to $1T, but private credit has also become a major player in it, as shown in the super confusing chart below.

You might be slightly puzzled about which line is relevant to us – Diversified Asset Managers or Credit Funds Specialized in SRT – and the answer is somewhat both. Although not explicitly described in the article, the “Asset Managers” category includes the Blackstones and Pimcos of this world because of their expansion into SRT-focused strategies, while “Specialized in SRT” includes some firms you’ve likely never heard of: Chorus Capital, Christofferson Robb & Co, and others.

The reason why both of these groups are relevant to us is that, over time, SRT has increasingly been viewed as a niche strategy within private credit, and the recent chart I used is proof of it (see lower right corner).

Aside from the fact that the private credit umbrella keeps expanding (asset-backed finance has only recently started being included in it on a more consistent basis), there is an interesting dynamic emerging around SRTs. The ECB raised this issue last year, and I covered it in Round #24: what happens if a bank provides back leverage to a private credit fund, and that same private credit fund, in turn, “insures” the bank’s loans via an SRT? For now, this remains largely a theoretical exercise because the data simply are not available and, in my view, diversification on both the banks’ and funds’ sides makes it a non-issue. But make no mistake, as funds’ investments in SRTs continue to grow, regulators will start asking these questions. And I will absolutely link this Round in a future letter and say, “As expected, they are asking these questions now.”

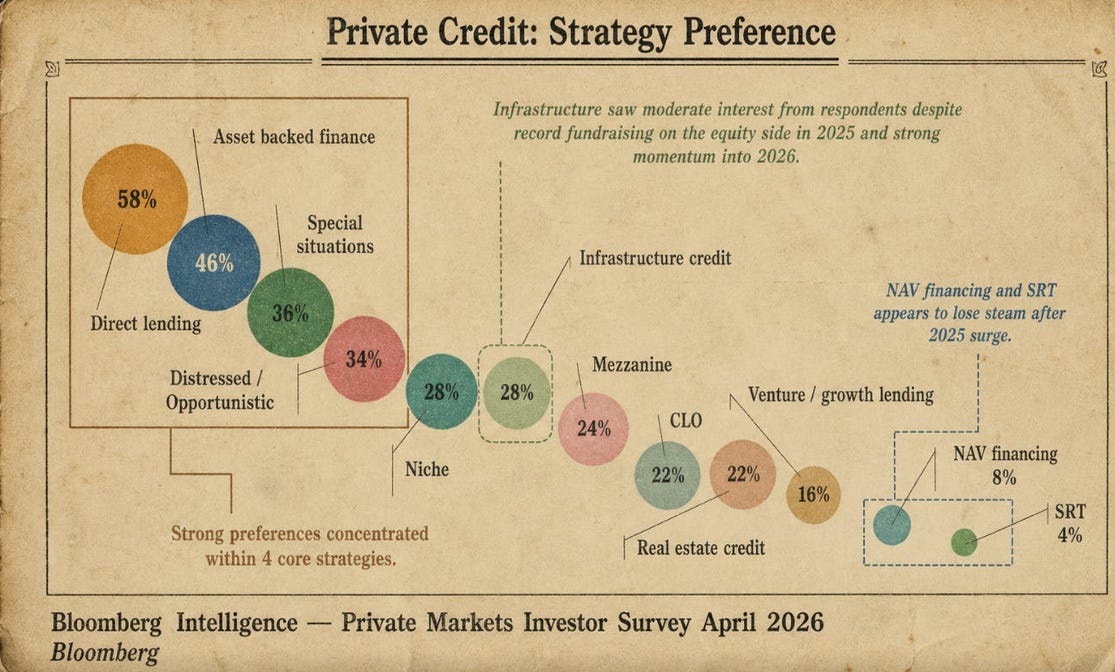

Lastly, if you are one of those rare people who are so interested in SRTs that you’ve tried to reconcile the $1T market size I mentioned earlier with the $25B or so in investments from various parties in 2025 (see the chart with Asset Managers etc. above), and couldn’t make sense of it… don’t. The $1T represents the total amount of all loans that are currently being “insured.” As you would know from my piece, typically 10-25% of a loan’s value, the junior piece, is insured (so, $100B-$250B). Since most bank loans have a 5-year tenor, you need to sum the investments over five years, which will likely be somewhat over $100B… so that’s the best I can do to reconcile the figures for you.

4. Apollo's Asterisk

Last week, Informa PLC held its famous private markets conference, SuperReturn, in Berlin, which typically attracts thousands of attendees because of its insanely stacked speaker list. One of the guest speakers was Apollo Asset Management co-president Scott Kleinman, whose remarks are featured in the Financial Times article Apollo executive says private equity got ‘a little out of whack’.

Btw, if you think you see Apollo in the media a lot, it's because they pull off some creative financing moves that raise some eyebrows, they call out other PE and PC firms' bad software bets and people love watching someone trash talk the industry, and slapping "Apollo" in a headline basically guarantees more readers (trust me, I see it in my own numbers).

Back to the article:

Scott Kleinman said there was a “collective assessment by fund investors saying the market got a little out of whack, and there’s going to be a price to pay as far as what that means for private equity performance for that 2017-22 vintage”.

Private equity firms have for years been struggling to exit deals struck at prices that can no longer be justified at higher interest rates, which have made the debt needed to fund buyouts more expensive.

Using “creative capital solutions” as an alternative to traditional exits “doesn’t solve the problem”, Kleinman said, but merely “ameliorates it and kicks the can for a later date”.

The Apollo executive insisted the firm had stayed “very disciplined on valuation” in its investments throughout the dealmaking boom.

I agree with Scott. I also have huge respect for Apollo, and think they are one of the top 2-3 alts, if not the top one. But I also find it mildly annoying how Apollo constantly dunks on the industry, almost implying, “We are better than these idiots.”

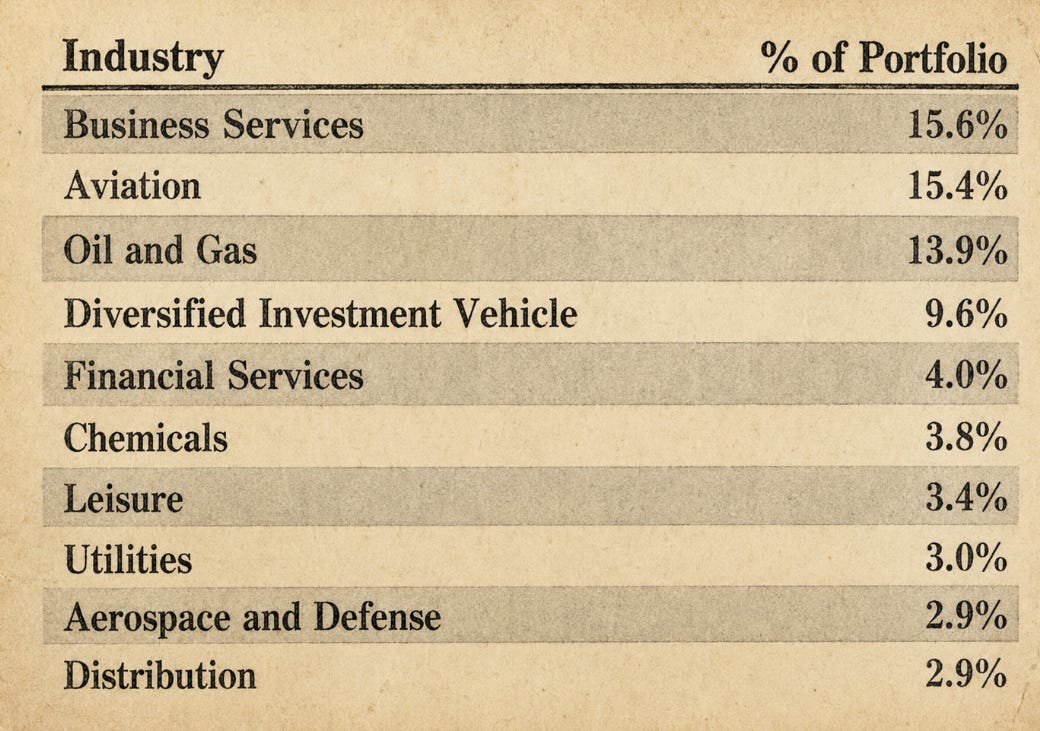

I think it is a fair criticism that PE firms used cheap debt to invest at top valuations particularly in software, which are asset-light companies with predictable subscription revenue (until recently, was considered manna from heaven). That said, the criticism sounds a little different when you remember that Apollo’s own BDC, Apollo Investment Corporation (AINV), hit a major bump in 2015-16 because of its fairly concentrated bet on capital-intensive Oil & Gas companies whose revenue was tied to the price of a commodity (about as far from manna from heaven as you can get). When oil fell from about $100 to $30s, driven by OPEC maintaining output while U.S. shale companies continued generating a lot of output, AINV felt the pain. Below is its industry concentration in early 2015.

You can see that Oil & Gas was one of the top 3 industries, which sucks when the sector runs into major headwinds. There are a couple of conflicting dynamics here that are not immediately obvious. On the positive side, some of these listed industries, such as chemicals, should benefit from lower oil prices (if oil is the primary input), creating a natural hedge against oil price fluctuations. On the other hand, if the Business Services bucket included vendors for oil companies, that's another source of stress.

Besides the sizable exposure to Oil & Gas, AINV's portfolio composition was also somewhat problematic, with only a minority of the portfolio invested in first-lien debt, while roughly half of its debt investments carried fixed interest rates, leaving the portfolio exposed to interest-rate fluctuations.

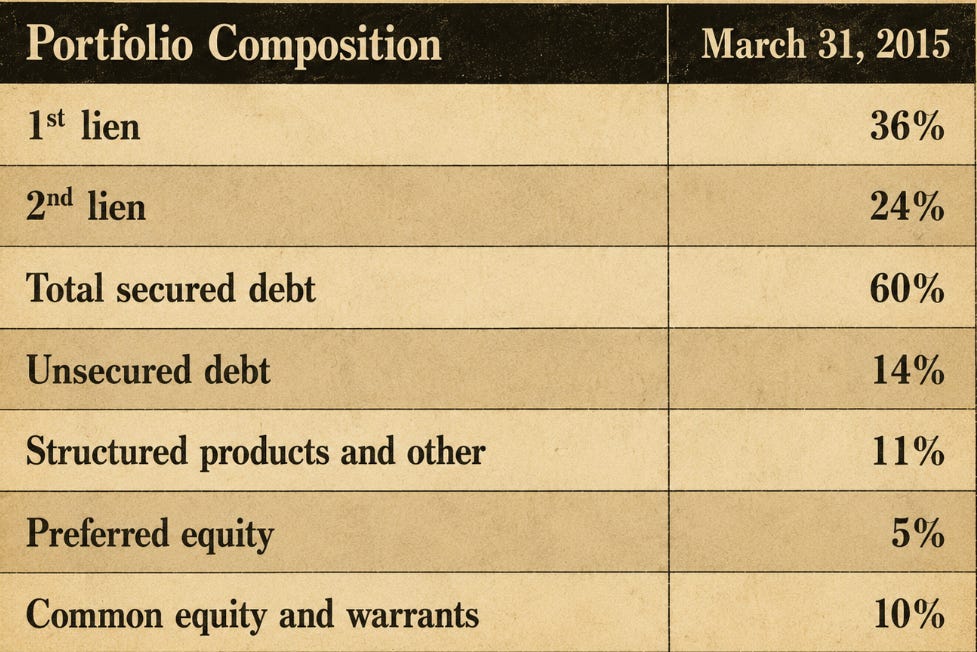

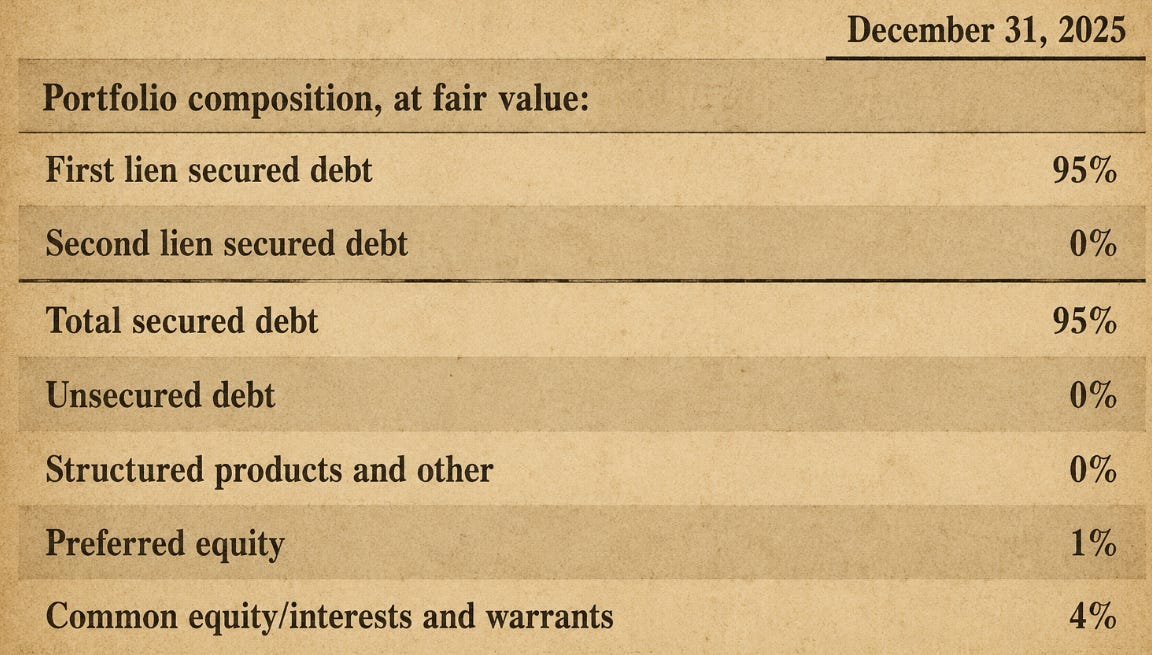

You might push back, saying that BDCs don’t necessarily have to be mostly invested in debt, and some are doing quite well with their more junior investments. I’d typically agree, but there is another twist to the story. At some point, Apollo realized that AINV was mismanaged and replaced management (great call), which subsequently changed the portfolio composition to the one shown below, suggesting that Apollo itself viewed the new approach as superior. The debt portfolio is now 100% floating rate (with no fixed-rate exposure). You know this BDC as MidCap Financial (MFIC); it was later renamed from AINV to MFIC.

The point of the story is that Apollo’s execs should tone the criticism down a notch, or at least include a disclaimer: “Having learned this lesson the hard way, [whatever they planned to say goes in here].”

5. Dividend Coverage Schmoverage

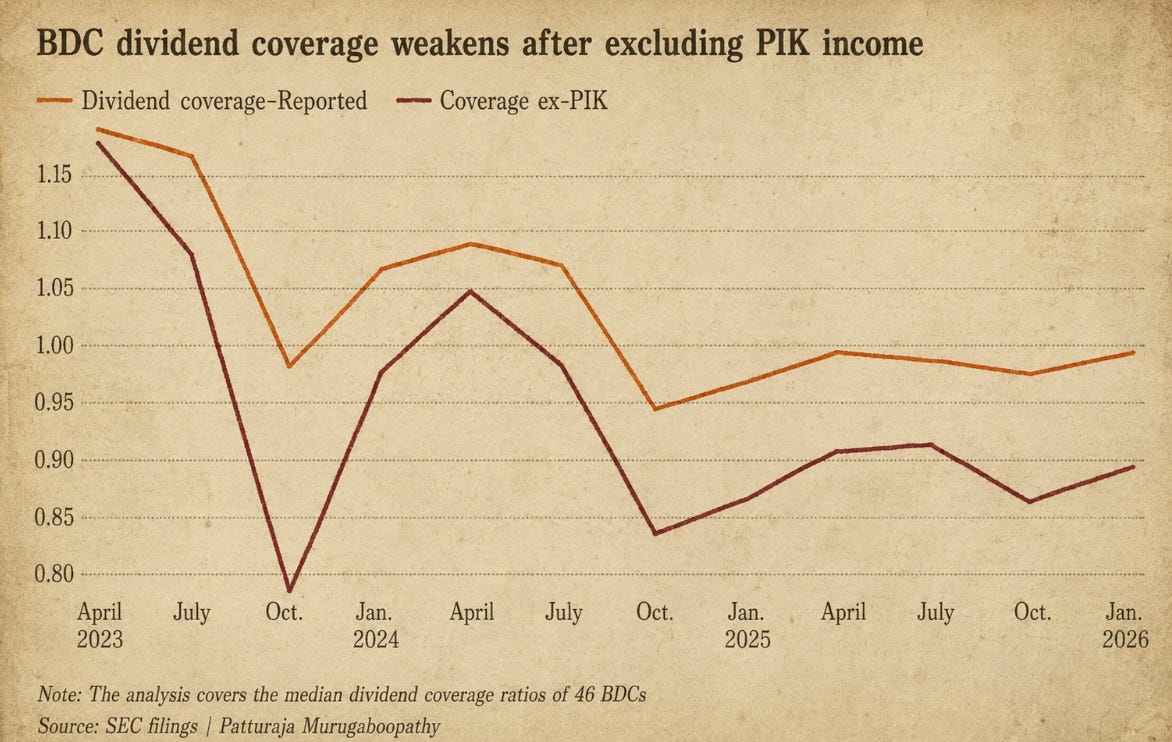

Reuters published a short piece on public BDCs’ ability to cover their dividends from earnings, which I thought was interesting. Not only because of what it found, but also because it made me pause and think beyond what was discussed in the article.

The paragraph below largely summarizes Reuters’ piece, and the chart under it provides a visual representation of the trend.

Median dividend coverage across 46 business development companies, or BDCs, slipped to 0.99x in the first quarter of 2026, meaning reported net investment income no longer fully covered regular and supplemental payouts. Excluding payment-in-kind interest, known as PIK, median coverage fell to 0.89x.

Coverage below 1.0x does not automatically trigger a dividend cut, as BDCs can use accumulated income or fee waivers to support payouts temporarily. But sustained shortfalls leave boards with less room to defend dividends if earnings weaken further.

There are a few things to cover here.

First, there is no such thing as a mandatory BDC dividend cut solely because dividend coverage weakens. The closest thing to a hard constraint is the 200% asset coverage requirement (debt-to-equity of 2:1), which limits a BDC's ability to incur additional debt if breached. It does not by itself require a dividend cut, but lowering the payout is one of the simplest ways to get back into compliance.

Second, besides fee waivers and accumulated income, BDCs can use debt to pay dividends.

Third, and importantly, even though cutting dividends is not an ideal solution, it is not some sort of taboo, despite the fact that most investors buy BDCs for their yield. When the Fed rate goes from 5.25% to 3.50% (dragging SOFR down) and intense competition among lenders compresses loan margins, total yield is hit from both directions. That alone, even without factoring in PIK income and non-performing loans, can be reason enough to adjust the dividend. The key is not to be the first one to cut it, I guess.

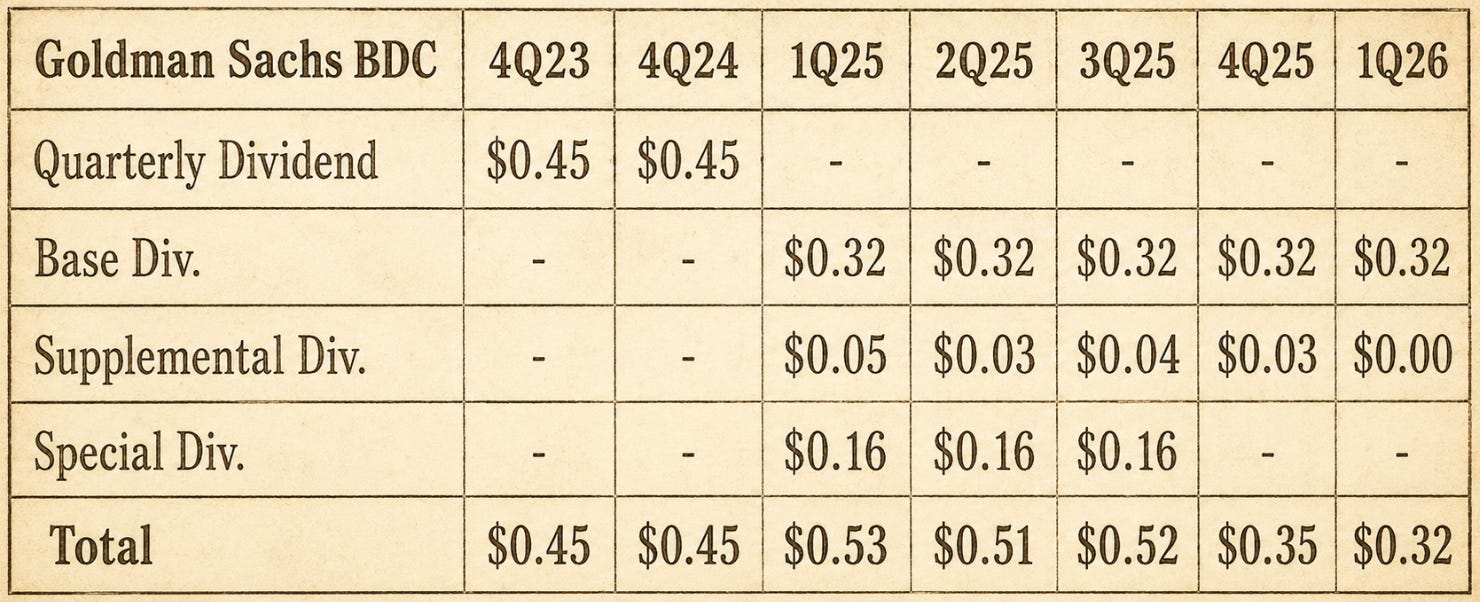

Also, it’s worth remembering how creative financiers can get when it comes to massaging the delivery of negative developments. Below is Goldman Sachs BDC’s dividend history over the past couple of years.

As you can see, historically, it paid a flat $0.45 quarterly dividend. In early 2025, however, Goldman declared a $0.32 base dividend, indicating that it expected to pay an additional $0.16 in special dividends over the following three quarters (clearly to soften the blow), along with a supplemental dividend. Base, supplemental, and special dividends are common not only in BDCs but in public companies in general, yet Goldman Sachs BDC had not used this structure previously (at least not during the prior two years).

What also helps soften the message is that BDC share prices have come down over the past couple of years, driven by noise around private credit, among other things. If you reduce a dividend while a BDC's shares are trading lower, the current dividend yield can still look solid (unless you've owned the BDC for a few years). For instance, at the end of 2023, Goldman Sachs BDC traded at approximately $15, and with an annual dividend of $1.80 ($0.45 × 4), the dividend yield was 12%. If you use today's $9.29 share price and annualize the Q1 dividend ($0.32 × 4), you get a 13.8% yield.

So, to summarize the piece, a lack of dividend coverage is not lethal, and a dividend cut can always be blamed on external forces and sanitized by skillful bankers who do that for a living.

6. Deals on the Block

Download below: the complete Excel file covering 50+ deals completed in 2Q26 (plus the prior two quarters).

Now, a word from our dear sponsor!

Buyside Hub ran Wall Street’s largest Compensation Report and has over 10,000+ compensation datapoints. Onboard to view the report here:

https://www.buysidehub.com/welcome

7. Bulletin Board

WSJ Online is offering 60% off its annual subscription to EMEA-based subscribers (€4 per month vs €10) and 65% off to U.S.-based subscribers ($4 per week vs $11). IDK why there is such a large price discrepancy…or a price arbitrage opportunity for EU-based readers? LINK

Bloomberg is offering 60% off its annual subscription ($180 vs $399). If you are in Business, Bloomberg is a MUST, with no real close alternative (LINK).

Shortcut.AI, an AI tool for Excel that lets you build models by simply typing requests (similar to ChatGPT). It is free to use up to a certain number of tasks per day (LINK). If you hit your limit before finishing your project, simply upgrade to the Pro plan ($20/month) and enter promo code DEBTSERIOUS (all capital letters) to get 50% off.

LoanEdge, a BDC research tool that lets you look into BDC loan compositions, individual loans, which BDCs own a specific loan, and more, is kindly providing DEBT SERIOUS readers with a free 3‑month trial (the regular price is ~$3k per year, and it’s higher for institutions). Here is a LINK to the tool. Send an email to Sadaf Khan at sadaf@theloanedge.com and let her know you are from the DEBT SERIOUS community.

As a reminder, I don’t personally benefit from either of these offers. I am just saving you money.

Lastly, our community is over 4,200 strong and includes a broad cross-section of mid- to senior-level professionals across private credit, private equity, LPs, and debt advisory. Please use the Bulletin Board at the end of each weekly letter to share events, discounts, or deals that benefit the community. I will continue to feature these opportunities and personally connect interested parties at no cost.

That’s the bell — round over. See you in the next.

Aznaur

Aznaur.Midov@KierLior.com

Section #2 was a great roundup of that story. The original BBG article didn’t provide the context you did, so thank you for that.

Section #5 was an excellent summary.