Round #46: Apollo + Blackstone: GPU-Backed Loans

KKR on Trading Loans; Apollo & Blackstone's $36B Loan; Loans to PE-Backed Companies in Decline; CDS on Hyperscalers; Defaults Reexamined; Faster Runs on Banks; Notable Deals; Bulletin Board.

In Round #46: KKR on starting to trade private loans; Dissecting Apollo and Blackstone's $36B loan to Anthropic; Decline in PE-backed financings; Looking into CDS market for hyperscaler debt; A take on the recent podcast on private loan marks; Banks to prepare for faster deposit flight; Notable deals; Bulletin board.

Disclaimer: there are 4,100+ of us here discussing private credit and leveraged loans, which is not a big world. At some point, I will probably throw punches at your company. I am blunt and sarcastic and, as friends like to remind me, too mouthy to live to an old age, so my take likely won’t please you. But don’t worry, next week it will be someone else in the spotlight and you will quietly nod along in satisfaction.

Also, none of this is investment advice.

1. KKR’s Maybe

Alright, so this Bloomberg article discusses KKR Co-CEO Scott Nuttall’s view that KKR will likely follow Apollo’s lead and start trading private loans.

Let’s see what Nuttall said (emphasis is mine):

The benefits are probably clear. It probably attracts more capital over time.

I think more transparency tends to be a good thing. It’s likely to happen over time for some types of private credit loans. Maybe direct lending could lend itself to it, but it’s early.

Is it just me, or does it sound like Scott isn’t into this whole "private credit trading" thing?

I don’t blame him. Why would you want to give up the single best thing about private credit, its opacity, which allows you to outperform public benchmarks, generate sticky fees, and avoid headaches of speaking with clients every time there is a market correction? I am being serious, because trading means you will actually have to mark these loans to market at the last price those loans were traded at.

Then again, investors clearly don’t have much faith in KKR’s marks in the first place, with one of its vehicles, public BDC FS KKR, trading at 0.58x NAV. For reference, BlackRock’s TCPC is also trading at 0.58x NAV, meaning investors have about as much faith in KKR’s marks as they do in those of a competitor who cut its NAV by 19% in one quarter and is being probed by DOJ. It takes talent to earn that level of trust... and that talent is really not sure if it wants more transparent pricing, you know?

Trading private loans obviously goes beyond public BDCs, which represent a small part of the private credit universe, and will affect drawdown funds (where LPs provide capital to credit funds to invest, typically locking it up for 10 years), and even life insurance companies, which have become sizable contributors to private credit funds, accounting for 30% to 40% of top alternative asset managers’ AUM.

As a side note, I frankly can’t wrap my head around why Apollo is pushing so hard for private loan trading. Like, come on, you are running a levered insurance company (Athene), which itself benefits from the lack of mark-to-market accounting.

My only explanation for this phenomenon is that Athene has become such an annuity-generating machine that there simply isn’t enough credit origination capacity to deploy all that capital at sufficiently attractive yields (after all, annuities guarantee roughly 4.5%–6%).

Or maybe I’m overthinking it, and Apollo just wants more transparency in this world...

2. Apollo + Blackstone: GPU-Backed Loans

Well, it’s technically TPU-backed financing and not GPU, but the latter is more intuitive. We’ll get back to it, because that’s actually quite an interesting theme that I personally haven’t spent much time understanding until I started trying to make sense of the article for the letter.

The article is Apollo Shops $36 Billion Debt Deal to Buy Google Chips for Anthropic and opens as follows:

Apollo and Blackstone are working to bring additional investors into a roughly $36 billion debt financing deal to help Anthropic build out its AI infrastructure.

The debt will be used to purchase Google’s custom chips called TPUs, or tensor processing units, which Anthropic will then lease. Broadcom, which helps Google develop the chips, is backstopping payments on the largest portions of the transaction.

Alright, I’ve heard of Google TPUs as an alternative to Nvidia’s GPUs (Graphics Processing Units), but that was the extent of my knowledge. I didn’t bother learning more because I assumed the AI bubble would burst before I could finish reading an article about TPUs. Obviously, I was wrong.

There is also this Broadcom dude in the mix, apparently willing to pick up the tab if Anthropic doesn’t pay. So, things don’t make a whole lot of sense as they stand.

Let’s dissect what’s going on here, and then return to the transaction itself.

Google’s TPU vs Nvidia’s GPU

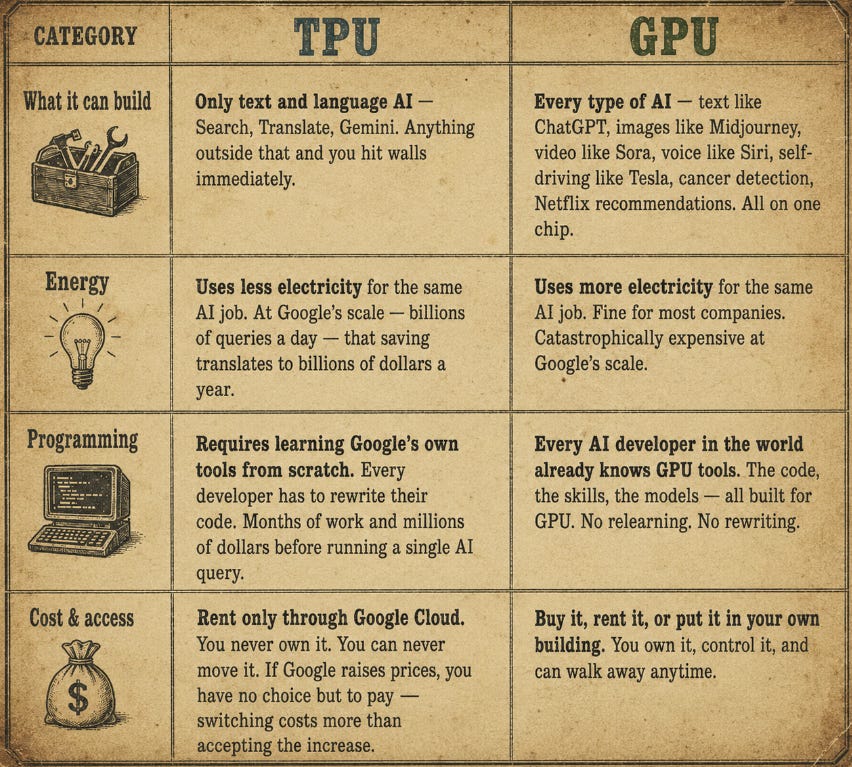

Long story short: back in 2013, when only like three people talked about AI, Google ran a calculation and realized it had a problem. If every Android user started using Google’s new voice search feature for just 3 minutes a day, the additional compute load would cost them billions. Back then, they were relying on GPUs. These are powerful chips originally designed for video games, movies, and other graphics-heavy workloads. The thing is, Google didn’t need most of that fancy stuff. It just needed a chip that could run AI models as cheaply and efficiently as possible.

So they basically said, screw it, let’s build our own. Instead of using a general-purpose chip, they designed one specifically for machine learning workloads. By cutting out all the unnecessary graphics functionality, they could run AI models faster, cheaper, and with much better energy efficiency. The result was the TPU (Tensor Processing Unit). By 2015, Google was already using TPUs internally, and in 2016 it officially unveiled them to the world.

Google didn't just start manufacturing TPUs though; it had partners. Google designed the chip from top to bottom, including all the software that runs on it, then brought in Broadcom to turn that design into something that could actually be physically built; and then sent the completed design of the chip to TSMC (Taiwan Semiconductor Manufacturing Company) to manufacture those chips. That's basically the flow, where Google pays both Broadcom and TSMC to create TPUs, but the chip belongs entirely to Google.

Below is a side-by-side comparison of TPU and GPU.

One quick note – that cost & access part; with Anthropic, it is actually changing, so someone else will own it.

Another quick note before we return to the transaction: Amazon and Microsoft started building their own chips for the same reason, named Trainium and Maia respectively. Both are behind Google, which has a decade head start. And guess who manufactures Amazon's chips? TSMC. Microsoft's? TSMC. NVIDIA's? TSMC!!! That is why you keep hearing about Taiwan on the news!

The Transaction

Historically, Anthropic used Amazon’s and Google’s data centers (or clouds, to be more specific) to train its models. However, late last year, the company announced plans to invest $50B in dedicated AI infrastructure, starting in New York and Texas (with Louisiana joining later). The goal is to reduce Anthropic’s dependence on third-party infrastructure while securing enough compute for future models. The current $36B debt raise is part of that project. Bloomberg suggests the TPU chips financed through this deal will be deployed across sites in New York, Texas, and Louisiana.

So, in this transaction, Apollo and Blackstone are financing the acquisition of TPU chips, which will be placed into an SPV. The financing is structured as a typical Asset-Backed Finance transaction, where the debt is sliced into multiple tranches: $6B of A1 notes, $25B of A2 notes, and $4.5B of B notes, which are then sold to investors (you can bet Athene will end up holding a decent chunk of the A-rated paper).

The interesting part of the structure, as noted above, is that Broadcom will provide a payment backstop for the chips. The article explains what that means (emphasis is mine):

That means that if Anthropic fails to make the lease payments for a certain period of time, the SPV will sell the chips to pay back the debt investors. If the value of the chips doesn’t make the debt investors whole, then Broadcom will make up the shortfall for 100% of the value owed to the A1 and A2 investors.

A few things to discuss here.

First, Apollo and Blackstone basically said: “Look, we love what you guys are building, but you are burning through cash like crazy and we are not comfortable holding $36B without someone guaranteeing these payments.” They obviously looked at Google first, but when there was no reaction, they went to Broadcom.

Second, Broadcom is an investment-grade company, which helps a lot. But why would Broadcom agree to backstop the payments? Because without the guaranty, there is no deal, which means a $36B chip order simply does not happen, and Broadcom misses out on the revenue it would have otherwise earned from this transaction.

Third, Broadcom is only on the hook for $31B out of $36B, covering the A1 and A2 tranches only. And even that overstates their real exposure. Broadcom only pays the difference between what the chips are liquidated for and that $31B. In other words, if the chips lose less than 14% of their value (1 - 31/36 = 14%), Broadcom pays nothing. The guaranty also covers a defined period of time, not in perpetuity.

Now, the question is: why didn't Google provide the guaranty when it stands to benefit the most from the $36B deal? Well, the article is focused on the chips angle only. Yet, typically, in data center construction, the actual real estate is also financed separately and placed into its own SPV. In Anthropic’s case, it has a contract with a company called Fluidstack, which engineers and operates data centers after they are built. Fluidstack doesn’t own the buildings; it leases them and then fills them with TPUs, cooling equipment, and everything else needed to run Claude. For the Louisiana data center, Fluidstack leased the actual real estate from a company called Hut 8. What happens if Anthropic relies on Fluidstack to run a data center, and Fluidstack can’t pay its lease to Hut 8? Anthropic suffers. As a result, Google provided a lease payment backstop for Fluidstack.

So it is fair to assume that in the current deal, Broadcom is backstopping the chip financing, while Google is backstopping the lease payments for the real estate structure.

Alright, moving on.

Time Out

So, there is a well-known FinTwit account called High Yield Harry, with an audience of more than 600k followers. Harry is a smart guy – he realized that if he could get some of his private credit/leveraged finance followers to anonymously share their compensation, he could end up building a pretty useful database. Thousands of people agreed, and that’s basically how Buyside Hub was born (or at least that’s my theory).

Anyway, Harry didn’t pay me to write any of that. But he did pay me to post the logo and a few lines below it (because I’m surprisingly easy to bribe), and you’ll see me mention Buyside Hub a few more times over the next month.

BTW, if I ran the company, the tagline would be: Buyside Hub – bringing you hard evidence that you’ve been underpaid.

Buyside Hub is a compensation analytics platform heavily used by Private Credit and Leveraged Finance professionals.

It is the one-stop shop for a detailed compensation breakdown for Buyside Credit professionals.

And it’s 100% free for those who join and contribute to the platform. You can join 15,000+ other Buyside Hub community members here:

3. PE Deals Out of Office

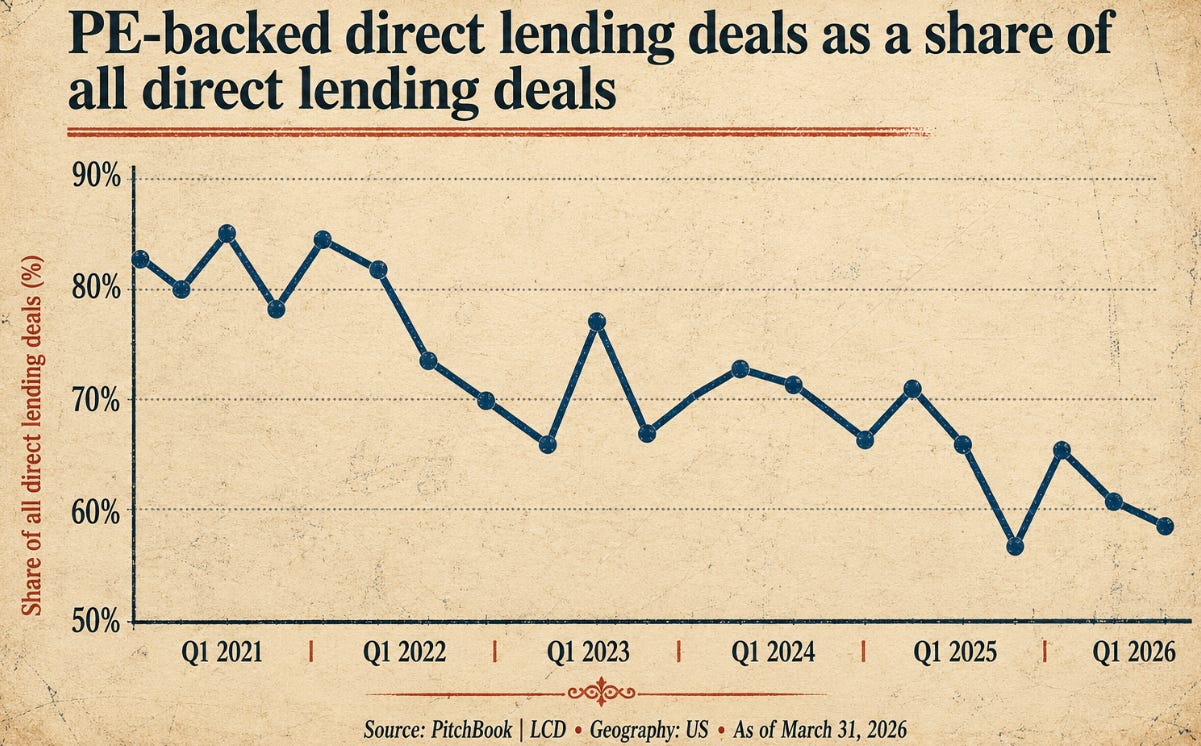

I came across this curious piece by PitchBook, PE-backed Companies Are Losing Their Direct Lending Dominance, which suggests that lenders finance fewer PE-backed transactions than in the past. It came with the chart below.

I initially thought that perhaps the author was conflating deal count with volume. We’ve started seeing direct lending deals with large public companies, so if we are measuring activity by dollar amount, surely one of those transactions is worth 10 traditional PE-backed deals. That was not actually the case, as the article clearly discusses deal count:

PE-backed companies accounted for roughly 6 in 10 US direct-lending deals in Q1, according to PitchBook LCD data, down from more than 8 in 10 during the post-pandemic deal boom.

This is very counterintuitive. Put yourself in the shoes of a lender who needs to deploy capital. Would you rather build relationships with a hundred LBO funds and finance the transactions they bring you, or source opportunities from tens of thousands of companies that may one day need financing? Both are oversimplifications, of course. With LBO funds, you will always compete with other lenders. And with direct deals, you would typically source opportunities through lawyers, IBs, and other intermediaries that already have relationships with borrowers (so you are not calling 1,000 CFOs). But the basic logic holds.

That said, there are private lenders who specifically focus on non-sponsored deals because they can get premium pricing, tighter documentation, and lower leverage. The obvious reason is that, unlike PE deals, there is no Debt Capital Markets person who knows the market, plays lenders against one another, occasionally threatens to never do business with you again if covenant cushions are not wide enough, and generally squeezes every last concession out of the lending group.

So, for a split second, I thought that maybe lenders had become tired of being bullied by these DCMs and moved toward direct deals.

I should have kept reading, though, because the explanation was just a couple of paragraphs below:

“The 60% right now is really being driven, not because there’s a lot of activity in non-sponsored—it’s because there’s not enough activity in sponsored,” said Dianna Carr-Coletta, managing director in the private credit team at $1.5 trillion asset manager PGIM.

Well, it seems that PE firms are simply doing fewer deals. And if I had to guess, historically they would buy new platforms, bolt on acquisitions, and eventually exit those investments (quite often to another PE firm). Today, however, we are seeing far fewer exits, something that has been widely discussed in the media.

Anyway, thank you for coming to my TED Talk about a phenomenon that didn’t actually exist.

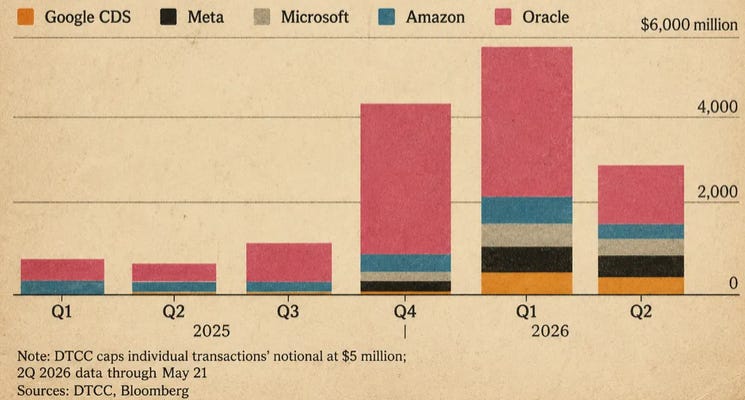

4. CDS Steps Up

Alright, going back to AI-related debt. Hyperscalers have already borrowed close to $250B globally to finance data centers, and most of that money comes from banks. Banks are regulated entities, and regulations cap how much any single bank can lend to one borrower, no matter how blue-chip that name is. At the same time, banks want to keep doing business with these strong borrowers. There are a couple of ways they can do this. First, Significant Risk Transfers or SRTs, which we touched on a couple of weeks ago. Second, CDS - credit default swaps, which we will get into below.

According to this Bloomberg article, hyperscaler CDS trade volumes have been picking up, with banks' hedging desks among the biggest buyers. The chart below shows exactly that.

Oracle is clearly everyone's favorite, perhaps because Ellison's baby is already ~5x levered with $135B of debt on the books. There is also a cute little line in Oracle's latest 10-Q that likely explains why its CDS is the most actively traded:

“As of February 28, 2026, we had $261 billion of additional lease commitments, substantially all related to data center arrangements, that are generally expected to commence between the fourth quarter of fiscal 2026 and fiscal 2028 and for terms of fifteen to nineteen years that were not reflected on our condensed consolidated balance sheets.”

So yeah, that's ~$15B of lease payments a year about to hit against $28B of EBITDA, although those same data centers should eventually juice the latter. But I digress.

The question is who is on the other side of these CDS trades? Hedge funds. Unlike banks, they are not regulated and they capitalize on no-brainers when they see one. The article elaborates:

“It’s the best opportunity in AA credit default swaps in a very long time,” said Andrew Weinberg, portfolio manager at Saba Capital, referring to the opportunity to sell protection on highly rated hyperscalers at prices typically seen for smaller, lower rated companies. “You are dealing with an inefficient market.”

Meta’s 5-year contracts traded on Friday at about 0.73% annually, meaning a hedge fund selling protection on $10m of principal can collect $73k. There’s relatively little risk: Meta is graded AA-, the fourth-highest level.

It’s far more lucrative than selling CDS tied to companies in the broader North American investment-grade index. A 5-year default protection on $10m of the index cost about $52k annually, and the index’s average rating is about BBB+, or four notches lower than Meta.

This is quite fascinating because investors typically choose between lower-yielding, higher-rated securities and higher-yielding, lower-rated ones, ultimately picking the one with the best risk-adjusted return. Here, that tradeoff doesn't exist because hyperscaler CDS offer both higher yield and higher rating simultaneously, making them an absolute no-brainer.

5. Defaults, Reexamined

Last week, I looked very hard for a great podcast to listen to... and found my own (which is pretty much how investors pitch themselves). But seriously, a few days ago, I published an episode with Ron Kahn, Co-Head of Global Valuations at Lincoln International, where we dove deep into private credit loan marks.

I don’t typically spend time discussing my interviews, but I found this one particularly educational because I didn’t really understand the nuances of the valuation process. Before getting into the discussion, a quick word on Ron: if you ever come across the terms “Bad PIK” or “shadow defaults,” chances are the source is one of his quarterly reports. His team coined those terms (at least in the case of Bad PIK).

Here are some of the topics we covered:

(i) what loan marks really mean; (ii) what loan marks indicate that equity is impaired (hint: not 90 and maybe not even 80); (iii) the valuation methods used to mark loans (fundamental and technical); (iv) the valuation process from beginning to end, including the role of private credit; and (v) the move from quarterly marks to monthly and even daily marks.

One thing we touched on briefly completely changed my perspective on defaults. Ron mentioned that they performed a study to estimate what a 10% default rate would mean for private credit investors. He walked through the assumptions, which, to be fair, sounded a bit optimistic, and the final results. I’m not here to agree or dispute the results, but to highlight a point that I, and many commentators, have been getting wrong.

Historically, private credit has returned about 10% per annum (plus/minus, but that’s not the point). Lincoln International’s studies show a 2-3% default rate, but when including Bad PIKs, the shadow default rate is 6%. So naturally, my math was: 10% return, minus 6% defaults, plus whatever is recovered. For simplicity, let’s just say nothing is recovered and every default leads to a full write-off.

So, I thought defaults could go up another 4% before the return breaks even (10% return minus 10% defaults), and that is the point at which we will have issues. To be clear, defaults need to almost double, and we need to assume no recoveries from those defaults, which is quite a grim assumption, but still possible. Anyway, all this makes sense, right?

Wrong!

This scenario suggests that a fund experiences 10% defaults and no recovery EVERY YEAR. In other words, 1 out of 10 loans in each year cohort goes bust, which would take an exceptional level of stupidity to achieve such a track record. In reality, that 10% is cumulative over several years: about 1% defaults in the first year, then, while you’re still working through those losses, another 2% defaults in the second year, followed by a major macro event that triggers 6–7% defaults, and so on. Defaults take some time to resolve, so eventually you get to that cumulative 10%.

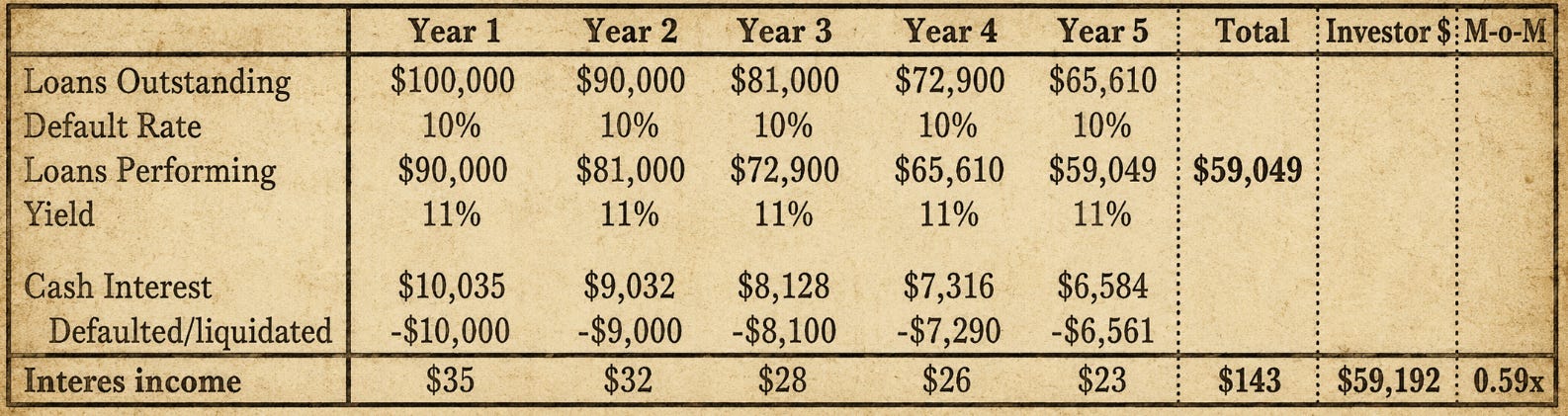

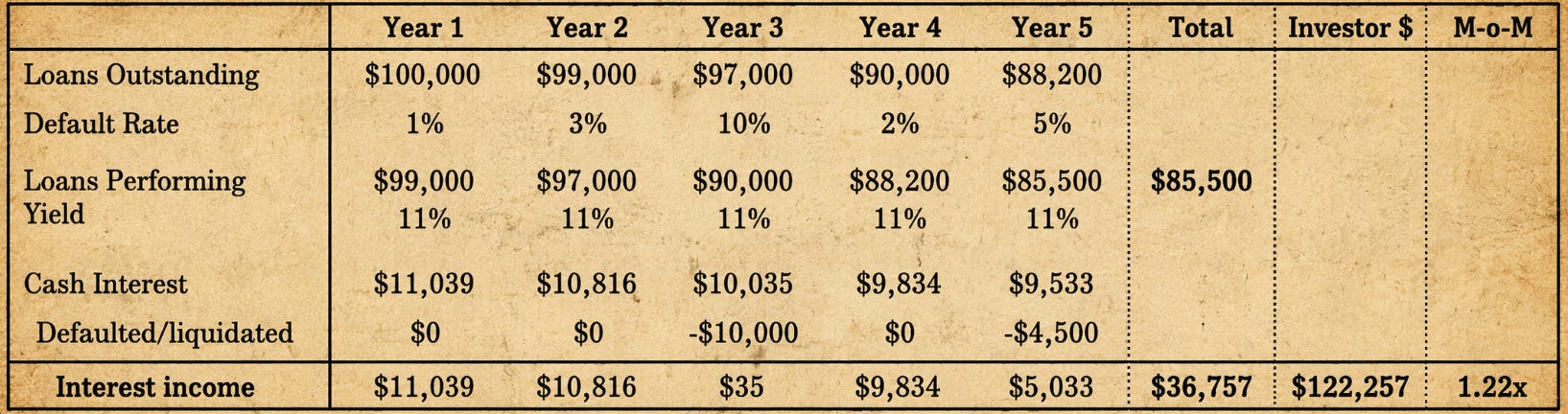

I am sure you conceptually understand what I mean, but to illustrate, below are two simplified charts. I didn’t add cohorts of loans, and instead assumed that a fund has $100m fully invested in a diverse set of loans. Each year, a percentage of loans defaults and stops paying interest (we ignore any expenses or other forms of fees, just interest income). At the end, we calculate how much investors get back in principal and total interest. Although typically funds last about 10 years, I’m using 5 years to match the most common loan tenor (5 years). Also, I used an 11% yield, because 10% was producing a negative return from the get-go and I didn’t want to overcomplicate the illustration.

One last thing – in the first chart, I write off defaulted loans each year as they occur, whereas in the second chart I let the loans accumulate before writing them off. It leads to pretty much the same result, but is more illustrative (it’s also a bit more punitive than doing it every year, but it’s immaterial).

So, the first chart is my initial assumption: “the problem will start when we get to a 10% default rate.” As you can see, performing loans continue declining 10% per year, and at the end the investor gets back $59m of principal and $143k in interest for a total of $59.2m. Relative to the initial investment of $100m, we are at 0.59x. You don’t need to be an expert to look at this chart and realize how little sense this makes. No one writes off 10% of loans a year, that would be wild. Also, this chart assumes that only $90m of loans were generating interest in the first year, effectively implying that 10% of the portfolio defaulted immediately after origination before making a single interest payment... (to be fair, BlackRock TCPC is probably thinking there is nothing wrong with that assumption…)

Now, below is a more realistic picture. Gradual defaults accumulate to 10% by year three (1% in year 1 + 2% in year 2 + 7% in year 3, giving us 10% cumulative defaults), followed by those non-performing loans being written off to zero. Then a new cycle starts with 2% defaults in year 4 and 3% in year 5 for a total of 5%, which is written off all at once in year 5.

As you can see, despite loans reaching a 10% default rate, the investors still made 1.22x on their initial $100m investment. I mean, that’s not what they sign up for. It’s merely 4% annualized, but it’s also not as catastrophic as you’d intuitively think. For what it’s worth, it still outperformed a very vocal private credit critic Jeffrey Gundlach’s return by a factor of 8x, although comparing the two strategies is admittedly apples to oranges (but I just couldn’t resist).

You can obviously be more punitive in the later years if you want, but the point is not to calculate the exact rate of return. Instead, it’s to realize that when you read headlines saying defaults are at 6% – that figure is cumulative and has accrued over at least 1-3 years. It doesn’t mean everything is fine. It just means the asset class has more capacity to absorb losses than I originally gave it credit for.

Anyway, if you want the same level of epiphany, listen to the episode with Ron Kahn (HERE).

6. Deposits Learned to Sprint

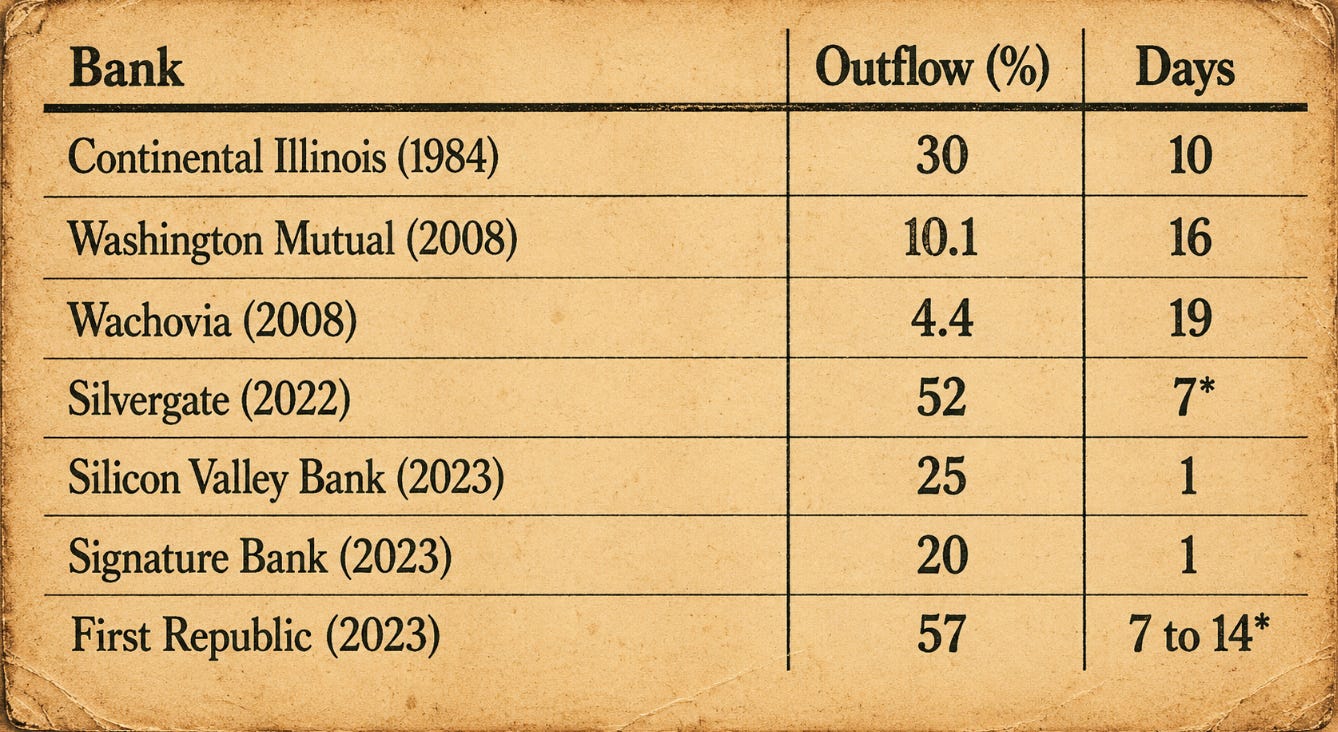

Bloomberg Editorial Board believes that banks need to prepare for high-speed runs. It’s a short but interesting read, with a few quick info digs needed to fully understand what they are saying.

The piece argues that while Silicon Valley Bank lost 25% of its deposits in a single day (and 87% within 2 days) three years ago, future panics could unfold even faster. Part of the reason is technology: AI could allow withdrawals to be executed automatically. Another factor is the rise of alternatives such as stablecoins, which give depositors more places to park their cash outside the banking system.

The piece includes a cool chart showing the percentage of deposits withdrawn over a given period during some of the largest bank runs in recent memory, and it looks wild.

After SVB’s 25% deposit withdrawal in a day, Wachovia’s 4.4% over three weeks looks like nothing. But remember that Wachovia wasn't just dealing with deposit outflows. It was also sitting on huge losses from its acquisition of mortgage originator (Golden West), a deal that blew up in Wachovia's face. So the run wasn’t the whole story.

Anyway, the purpose of this Bloomberg piece was not just to scare banks with the possibility of a future run that could put one out of business in hours, not days. It also proposes one idea to at least partially address the problem.

There is a mechanism available to U.S. banks as a source of emergency liquidity: the Federal Reserve Discount Window. The way it works is that banks pledge qualified collateral, and the Fed advances funds against that collateral. There are a couple of issues, though. First, it takes time for the Fed to evaluate the collateral, so unless a specific asset has been pre-pledged ahead of time ("prepositioned"), the funds may not be immediately available. Second, while prepositioning collateral with the Fed is not necessarily disclosed in filings, there has historically been a stigma around it, to the point where if the market were to find out, it might itself trigger a run on a bank.

SVB didn't have that set up, perhaps because of the stigma, and since then voices have become louder about addressing the issue. The proposal is that instead of the current requirement of having liquidity sufficient to cover an estimated 30 days of deposit withdrawals, banks should be required to preposition assets and set up access to the Discount Window. The point is that a universal requirement would destigmatize Discount Window usage.

Another point is... how can a bank keep 30 days of cash on hand when SVB lost 87% of its deposits in two days? Obviously, the Discount Window won't save a bank from such a massive run, but it would certainly be more effective than relying on the current setup.

Anyway, that’s the whole story.

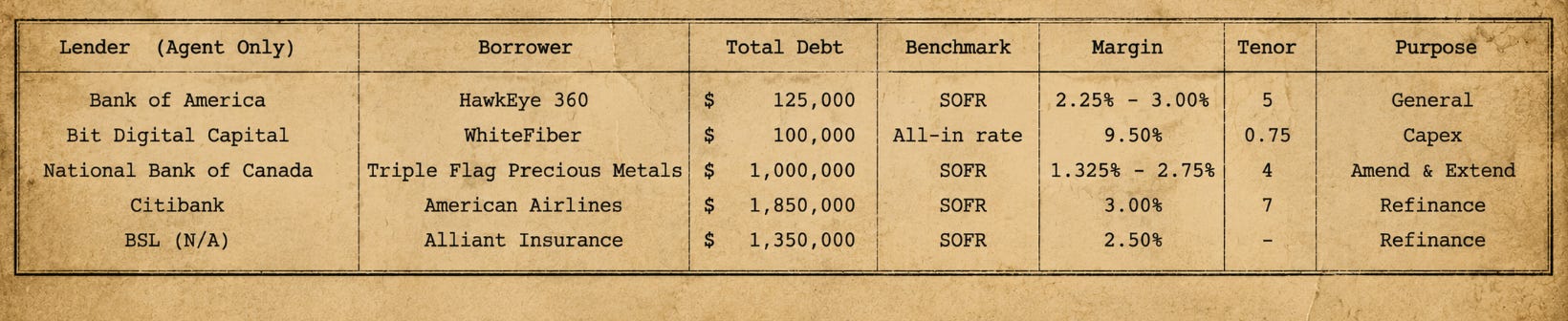

7. Deals on the Block

Download below: complete Excel file of all Q2 deals with details

8. Bulletin Board

Bloomberg is offering a 60% off its annual subscription ($180 vs $399). If you are in Business, Bloomberg is a MUST, with no real close alternative (LINK).

Shortcut.AI, an AI tool for Excel that lets you build models by simply typing requests (similar to ChatGPT). It is free to use up to a certain number of tasks per day (LINK). If you hit your limit before finishing your project, simply upgrade to the Pro plan ($20/month) and enter promo code DEBTSERIOUS (all capital letters) to get 50% off.

LoanEdge, a BDC research tool that lets you look into BDC loan compositions, individual loans, which BDCs own a specific loan, and more, is kindly providing DEBT SERIOUS readers with a free 3‑month trial (the regular price is ~$3k per year, and it’s higher for institutions). Here is a LINK to the tool. Send an email to Sadaf Khan at sadaf@theloanedge.com and let her know you are from the DEBT SERIOUS community.

As a reminder, I don’t personally benefit from either of these offers. I am just saving you money.

Lastly, our community is over 4,100 strong and includes a broad cross-section of mid- to senior-level professionals across private credit, private equity, LPs, and debt advisory. Please use the Bulletin Board at the end of each weekly letter to share events, discounts, or deals that benefit the community. I will continue to feature these opportunities and personally connect interested parties at no cost.

That’s the bell — round over. See you in the next.

Aznaur

Aznaur.Midov@KierLior.com

In the long term, Google will eat Nvidia's cake with it's TPUs. The are specialized for matrix multiplication which is was AI and ML algorithms are all about under the hood.

Excellent content. So many worthwhile threads here, but I will focus on a few points.

1. Your interview with Ron Kahn at Lincoln was top notch. Many podcasts have a low takeaway ratio. This one was choc a bloc with nuggets. And you did an excellent job of keeping it on track and pinning Ron down on the critical questions. It was a quality look into the valuation process. It made me slightly more comfortable (especially the part where he said the client nearly always uses Lincoln's valuations - albeit a range is provided and Lincoln allows input from the client - so somewhat more comfortable, but there is room for games).

2. A lot of Athene's growth has been funded by Funding Agreements lately, so they have become less reliant on annuities. This is hot money that can turn on a dime if Athene runs into trouble. It may also present an A/L mismatch risk to the extent the FAs roll off faster than the assets.

3. The Broadcom backstop on the $36B Apollo/Deal. As I have written about on the Meta data center financing, the rating agencies are allowing the guarantee to influence the rating of the data center debt, yet ignore the impact of the guarantee on the rating of the guarantor (eg Meta, Broadcom). I'd be curious to see how they justify this in the Broadcom case.

And yes, the only easy way Apollo can clear that kind of debt is using Athene's balance sheet. How else can they compete with Wall Street's distribution engine? At some point the concept of Glass-Steagall will be applied to insurance companies.

Though the debt may be disappeared in one of Apollo's nesting doll vehicles like AMAPS or the Fox Hedge LP. (I wrote about these recently).

4. I have a BDC tool (which I won't share here). It's currently free. DM me if interested. A lot of time spent developing additional data points and normalizing the data.

5. Regarding CDS being used to hedge AI debt - on its face, this looks like a tool that is serving its intended purpose. What NOBODY is talking about, is the regime shift in how CDS are cleared since the GFC. Trillions of dollars of risk are being transferred and nobody is talking about how these transactions are cleared and settled and risk managed.