Round #30: SaaS Loans: Different Angle

BOE and ECB Rates; A Deep Dive Into the SaaS World; Notable Deals; Bulletin Board

In Round #30: BOE and ECB rates update; AI and SaaS: implications for private equity and private credit; Notable deals; Bulletin Board

1. Five Percent Club

So, last week, the ECB left its interest rate unchanged at 2.00%, and economists expect it to stay around that level through 2027. During the same week, the BoE also left its interest rate unchanged at 3.75%, but the decision was just one vote away from a cut (a 5-4 split), signaling a potential reduction soon. This is all good news for the private equity firms that raised $400B and private credit managers who raised over $100B during the past two years to be deployed in Europe.

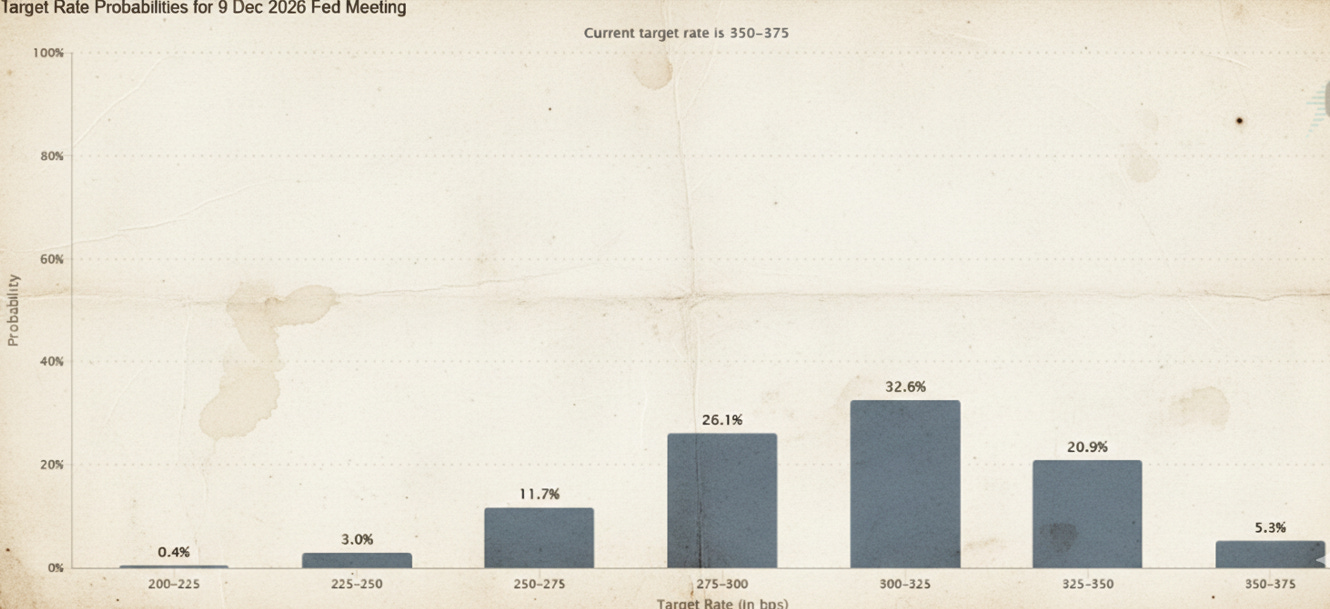

As you know, the Fed recently kept the rate unchanged at a target range of 3.50% to 3.75%, although everyone expects there to be cuts eventually (see chart below).

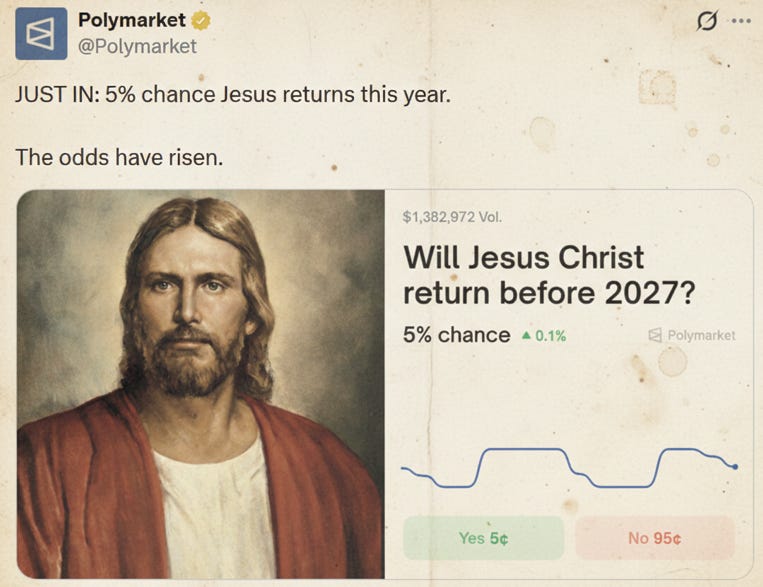

Essentially, there is a 95% chance the rate will be cut at least once this year, which is positive news for private markets as we have discussed many times. The chart also suggests there is a 5% probability that the rate stays unchanged. Coincidentally, that 5% figure matches the recent odds on Polymarket for the return of Jesus Christ this year.

I am not suggesting a direct correlation between monetary policy and the second coming, but I cannot confidently say they are unrelated.

2. SaaS Loans: Different Angle

Last week, Anthropic’s release of the "Claude Cowork" plugin marketplace triggered a massive sell-off across the software sector. By introducing specialized AI agents for legal, finance, and marketing, Anthropic fueled the sentiment that "AI will eat software". This shift is no longer just hitting equity valuations; it has spilled over into leveraged loans and is now impacting alternative asset managers with heavy software exposure.

I know you have already read dozens of takes on SaaS disruption and private credit’s exposure to it over the past few days. I was tempted to skip the topic altogether, but since I spent the later part of my career dealing specifically with SaaS loans and even hosted a podcast about SaaS, I started digging in.

I began speaking with people and organizing my own thoughts because it felt like events were moving too fast for anyone to form a nuanced view. After conversations with four SaaS‑focused lenders, a SaaS‑focused PE firm, and three consultants (and countless articles and papers), I arrived at a view that largely runs against the main narrative. There are really three separate angles to cover: (i) the consequences for SaaS; (ii) for private equity; and (iii) for private credit.

As I was putting together pieces for this week’s newsletter, I received a Substack letter, Don’t Short SaaS, a collaborative post between Les Barclays and Strategist. It is perfectly consistent with my “SaaS vs. AI” take but covers much more ground. I will leverage a few bits from it here, but also provide some additional background on the evolution of SaaS because there are certain parallels with AI dynamics. You can then go dive into their piece.

Software-as-a-Service

The term SaaS is often used loosely, but in its strict sense it refers to software that combines two characteristics: it charges a recurring subscription fee rather than a one-time license, and it lives on a central server (the “cloud”) instead of on-prem. While SaaS is now the default delivery model for business software, it began in the mid-90s as a niche corner of the tech ecosystem.

The real inflection point came in the mid-2000s with the launch of Amazon Web Services (AWS). Before AWS, building software was capital intensive. You needed physical hardware, database licenses, and development tools, which amounted to roughly $100k in upfront investment in today’s terms just to begin. Distribution was equally heavy. If a client wanted to use your software, they had to purchase and maintain their own servers (dedicated machines for storage and processing) where the application would live.

Many regulated companies still have “server rooms” for this reason. These rooms typically house software containing highly sensitive data, since some organizations remain uncomfortable with the cloud. In that era, software development was far less flexible. Fixing a bug could mean mailing physical disks or manually reinstalling the application on every individual machine. Updates were slow, expensive, and operationally painful.

Cloud computing changed that structure entirely. Led by AWS and later joined by Google Cloud and Azure, these platforms began offering Infrastructure (IaaS) and Platforms (PaaS). In practical terms, this meant developers no longer needed to manage hardware themselves. They could build software using third-party infrastructure that handled storage, compute power, and scaling behind the scenes. At the same time, customers no longer needed their own physical servers because the software lived on the provider’s centralized infrastructure.

The economic impact was dramatic. Upfront costs to build software collapsed. Updates could be pushed instantly to a central environment rather than installed one machine at a time. Bug fixes became seamless and invisible to end users. What had been a capital-intensive, operationally rigid model became scalable and asset-light.

This shift triggered a wave of new software companies. Venture capital flowed in, funding businesses that could scale rapidly without heavy infrastructure spending. A competitive battle emerged between SaaS providers and traditional on-prem incumbents. On-prem vendors dismissed SaaS as a fad, while SaaS advocates argued that legacy systems were structurally obsolete. The public rivalry between Oracle and Salesforce became the symbolic clash of these two models.

Adoption, however, was gradual. The primary concern was data security. Many companies feared that storing information in the cloud would expose them to commingling risks or cybersecurity vulnerabilities. As a result, SaaS first penetrated non-critical functions such as marketing and collaboration tools, while core financial systems remained on-prem.

By around 2015, the direction was clear. SaaS had become the dominant model for CRM, HR, procurement, and other enterprise tools. The final acceleration came during COVID, when remote work made centralized, browser-based systems not just convenient but necessary. What began as a niche delivery model in the 1990s turned into a 15 to 20 year structural transition. Today, roughly 85% of business software is delivered through SaaS.

“Anyone can create software,” “disruption of the incumbent,” “security concerns,” and “gradual adoption.” History repeats itself, doesn’t it?

SaaS Numbers 101

Before moving on, it is worth looking at SaaS from an operational standpoint. The model is unique, frequently misunderstood, and central to this discussion. If you already live and breathe SaaS, you can skip ahead. For everyone else, here is a simplified breakdown of the metrics that actually matter.

Historically, SaaS companies optimized for the top line rather than the bottom line because they were valued on revenue multiples, not EBITDA. The anchor metric is Annual Recurring Revenue (ARR), which represents the annual subscription revenue a customer is contractually committed to pay.

Think back to buying Windows XP on a CD. If it cost $120, Microsoft could recognize the full $120 as revenue immediately. Under a current $120 Microsoft 365 subscription, the cash may still be collected upfront, but revenue is recognized ratably at $10 per month. That means $10 in January, $20 by February, and the full $120 only by December 31st.

Because of this ratable recognition, ARR becomes the core valuation driver. The larger the ARR base and the faster it grows, the higher the multiple the market is willing to assign. We will come back to valuation later.

The second critical metric is Retention. Having $120 of ARR is meaningless if customers cancel after one year.

There are two retention measures. Dollar retention tracks how much revenue from the same customer cohort remains after a year. Client retention tracks how many customers renew. They sound similar but capture different dynamics.

Using the same Microsoft example, assume you later add four additional Microsoft 365 licenses for your family members for $480. Microsoft’s ARR from your household increases to $600. The additional $480 is upsell. If the following year you cancel two licenses worth $240, ARR drops to $360. That reduction is downsell.

Microsoft treats your household as one client. Even after cancelling two licenses, client retention remains 100% because the account is still active. Dollar retention, however, falls to 60% ($360 divided by the original $600). If you cancel entirely the next year, both client and dollar retention fall to 0%.

In practice, SaaS companies focus heavily on dollar retention, specifically Gross Revenue Retention (GRR). The “gross” distinction matters because it excludes upsell and only measures what was retained before expansion. Net Revenue Retention (NRR) includes both upsell and downsell and is often the more powerful indicator.

NRR measures how much ARR remains from the existing customer base after accounting for expansions and contractions, but excluding new customers. In the earlier example, adding $480 with no churn would mathematically produce a very high NRR (400%). In reality, healthy SaaS companies aim to keep NRR above 100%, which means they can grow even without signing a single new customer.

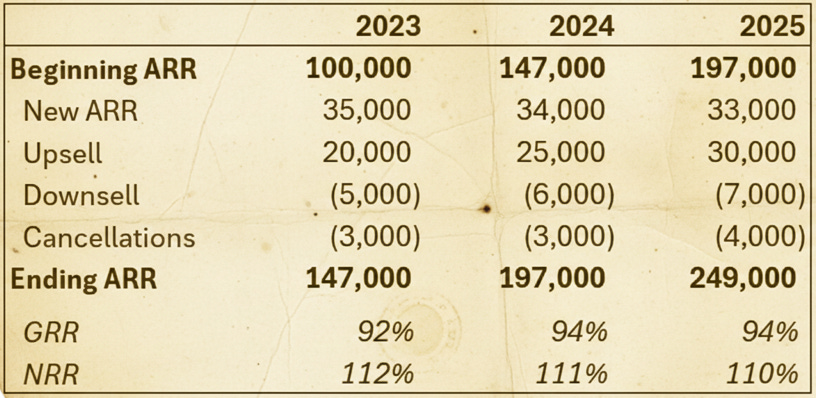

Below is a more realistic example of a SaaS company’s retention metrics.

A few structural characteristics of SaaS are also important for this discussion:

Historically, SaaS followed a per-seat, per-year pricing structure, which created predictable revenue because pricing was fixed. More recently, many companies have shifted toward usage-based or consumption pricing, where revenue fluctuates based on activity levels.

Contracts are typically prepaid annually, providing meaningful upfront cash flow.

Revenue is recognized ratably while expenses are recognized as incurred, creating a timing mismatch. As a result, EBITDA can understate true cash generation, and fixed charge coverage based on traditional EBITDA can appear artificially weak.

Lenders and sponsors often focus on “Cash EBITDA,” which adds the Change in Deferred Revenue to EBITDA. When customers prepay, cash is collected before revenue is recognized, and the unearned portion sits on the balance sheet as Deferred Revenue. As revenue is recognized over time, Deferred Revenue declines. The period impact is captured by calculating the year-over-year change in that balance.

SaaS businesses typically generate gross margins around 80%, but companies reinvest heavily in R&D and Sales and Marketing to drive ARR growth, which can make traditional profitability metrics misleading.

SaaS companies are intensely data-driven. Metrics such as churn, expansion, and customer acquisition cost are continuously benchmarked and monitored.

Artificial Intelligence Large Language Models

We are now getting to the core issue: AI-driven disruption of SaaS sentiment. While more thoughtful pieces are starting to argue that the threat is overstated, and I largely agree, the dominant narrative in markets remains that AI will wipe out large parts of SaaS.

Before going further, it helps to clarify what we are actually talking about. ChatGPT, Claude, and similar foundational models are a subset of AI known as Large Language Models, or LLMs. These systems are trained on vast amounts of text data. As I noted in a previous letter, an LLM is essentially a glorified memorization machine. It predicts the most likely next word based on patterns it has seen before. Because they have absorbed enormous portions of the internet, they are extremely useful.

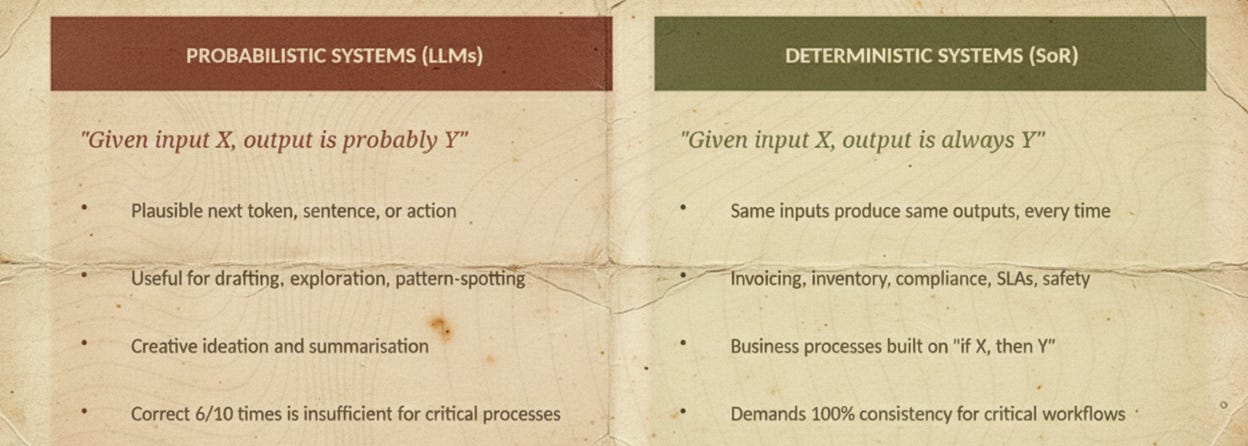

However, memorization is not reasoning. LLMs do not truly understand context. They generate outputs based on probability, not computation. That is why they are described as probabilistic systems. This probabilistic nature is their core limitation and the primary reason they struggle to replace certain categories of software. We rely on software as our system of record, and our approach to working with it is fundamentally different from how we work with LLMs.

The Don’s Short SaaS piece includes a comparison chart that illustrates this difference clearly.

A few points are worth highlighting.

“Correct 6/10 times” refers to general-purpose LLMs such as ChatGPT. There are vertical models that claim 80% to 95% accuracy within specific domains, but they remain probabilistic.

“Inconsistency” is not explicitly shown on the chart. If you ask the same question twice, especially in different sessions, you may receive slightly different answers or completely different outputs.

None of this implies that software will not be disrupted. It simply suggests that certain categories of software, at least in their current form, are not easily replaced by probabilistic tools.

To simplify the distinction, imagine your boss shouting across the office and asking you to build a table in Excel while speaking quickly. You think you understand what he wants, but you are not entirely sure. You hesitate to ask a follow-up question because you do not want to look dumb. So you build something that seems directionally correct and send it back, hoping it was what the boss asked for. That is how a probabilistic system behaves. It approximates the request based on patterns it has seen before.

In a deterministic system, by contrast, the boss sits next to you and walks through each instruction step by step: “Open Excel. Add revenue in cell A2.” He oversees every action until the task is complete. In that case, there is no ambiguity about the output because every step is defined.

Consistency is the other key issue. If you ask an LLM the same question multiple times, particularly if the prompts are issued in separate sessions, you may not get the same answer. For example, I asked ChatGPT to write a detailed description of a celebrity’s face. I then pasted that exact description into Gemini to generate an image. Repeating the process with identical wording produced slightly different outputs (below). In one version, the guy in the image was smiling. In another, he was not. Even though the description was identical, the result was not. If you repeat the exercise several more times, you are likely to get a different person altogether or even a response saying the model cannot comply with the request. For drafting an email, that variability is harmless. But for filing documents with the SEC, it is a problem.

Oh, by the way, for the image above, I asked ChatGPT to provide a description of Tom Cruise… just FYI.

There is another limitation that is easy to miss. LLMs are text models. They do not actually calculate. If you ask one what 2+2 equals, it will answer correctly, not because it is doing math, but because that answer appears everywhere in its training data. Ask it to multiply large numbers that were unlikely to appear in that data, and errors become much more common. The model is predicting the answer, not computing it.

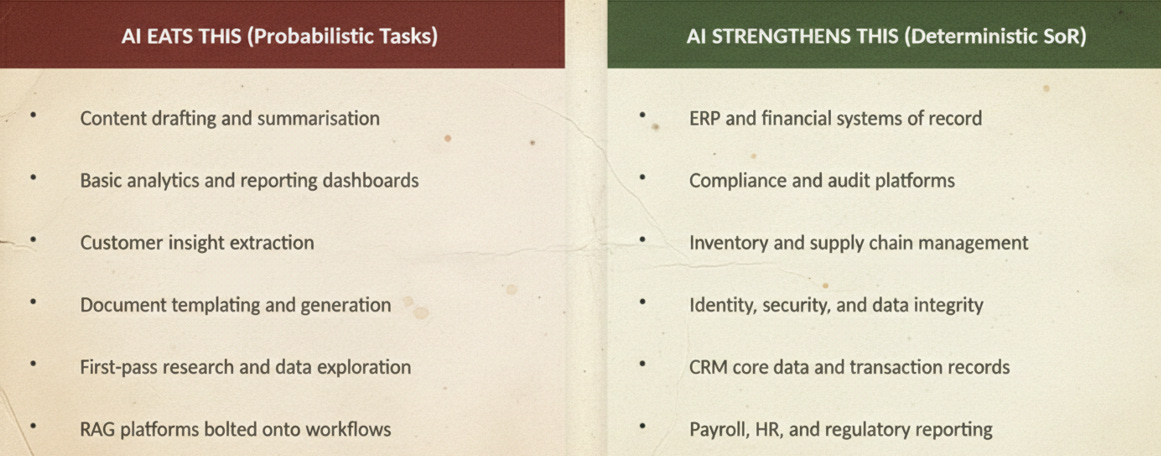

This does not mean LLMs will not disrupt software. Some product categories are clearly vulnerable. At the same time, other categories may become stronger by integrating LLM functionality. The following chart breaks this out in more detail.

There is also a quote in the piece that sums it up quite well:

As UncoverAlpha put it in his analysis of SaaS unbundling: AI will eat the probabilistic category, while deterministic systems become more valuable by integrating AI as a complementary layer. That framing is exactly right. When enterprises deploy AI agents in 2025 and 2026, they’re not replacing their systems of record. They’re building orchestration layers on top of them. CIOs are discovering that LLMs lack the deterministic consistency required for critical industries. A system that provides the correct answer six out of ten times is insufficient when the process demands 100% consistency.

The likely path forward mirrors the history of SaaS itself. LLMs will first gain traction in non-critical functions such as marketing and collaboration. Core financial and operational systems will remain anchored in traditional software platforms. For AI-native products to fully replace those systems, they would need to embed their own deterministic system of record on top of existing infrastructure. In other words, they would need to become AI-first platforms with a true SoR attached.

Private Equity

There are a handful of prominent SaaS-focused PE firms, but Vista and Thoma Bravo hold the title of pioneers, with Vista likely being the first. A quick sidenote: as I was looking into this, I realized that GTCR stands for Golder Thoma Cressey Rauner. This means Carl Thoma was behind both GTCR and Thoma Bravo… Good for him.

It is easy to see why private equity loves SaaS. The economics are ideal for leverage: recurring contractual revenue and 80% gross margins. This profile provides optionality, allowing owners to either aggressively invest in growth or manage the bottom line for cash flow.

The value creation playbook is well established. You buy a platform while it is small, say at 5x ARR, professionalize management, and execute a series of acquisitions. This strategy generates returns through a powerful trifecta: multiple expansion from increased scale, broader market demand for software assets leading to further multiple expansion (ZIRP anyone?), and leverage.

The chart below visualizes the historical valuation multiples for SaaS companies. It combines historical data from Alex Clayton and and more recent market data from Jamin Ball. These are public comps, which are generally larger and trade at higher multiples than private peers. Valuations are based on NTM revenue rather than ARR, since public companies do not consistently report ARR (non-GAAP metric).

As you can see, the only period when public SaaS traded at lower multiples than today was during the financial crisis.

Let’s revisit the ARR rollforward example from earlier. Although the numbers were hypothetical, it accidentally resembles a strong target for a large SaaS-focused PE firm.

They would have preferred to buy it in 2022 when ARR was $100m, leaving more runway for growth. But even at $250m ARR, the profile remains attractive for several reasons.

Scale. Of the tens of thousands of SaaS companies globally, only a few hundred have crossed the $100m ARR threshold. Beyond being rare, companies at this level are resilient. It is difficult to kill a SaaS business once it surpasses even $30m in ARR. Vista famously suggested that software contracts are better than first-lien debt, because companies will pay their software bill before their interest bill just to keep operating.

Growth. Combining that scale with 25%+ top-line growth is impressive.

110% NRR: A Net Revenue Retention rate above 100% means the company can grow 10% annually from its existing customer base without signing a single new customer. While high-growth public or VC-backed firms might post 120% or higher, 110% is solid at this scale.

94% GRR: A Gross Revenue Retention rate at that level implies minimal churn and limited downsell. We will double-click on this metric below.

While sponsors often focus on NRR, a GRR in the mid-90% range is very telling and typically signals mission-critical software. It means customers rarely switch providers. High switching costs and long implementation cycles make those products hard to replace.

Not surprisingly, many of those mission-critical solutions fall into the category of deterministic systems. The chart below revisits those types of solutions:

In an ideal world, most of a PE portfolio would consist of those mission-critical systems, which are less vulnerable to AI disruption. In reality, there are only so many CRMs and ERPs available. At the same time, there is effectively unlimited capital. That imbalance pushed many firms into segments that may be more exposed to LLM-driven disruption.

Timing made it worse. A significant portion of these investments were executed during the COVID-era valuation surge. The Fed interest rate hikes of 2022 and 2023 hammered valuations. AI-driven sentiment has since compressed multiples further. That dynamic makes exits difficult, especially for funds approaching the end of their life cycle. Expect more Continuation Vehicle (CV) transactions, including “CV squared” deals where one CV sells to another CV.

While this primarily impacts existing portfolio companies, my conversations with a SaaS-focused PE investor suggest that a few new avenues have opened up to deploy dry powder:

Take-privates: Large SaaS-focused PE firms have spent months submitting Indications of Interest to public SaaS companies at roughly 30% premiums across the board. An IOI forces a board discussion and can unlock additional diligence access. Many of these funds have had their finger on the trigger for some time, waiting for the right entry point. With public multiples compressed, the trigger is easier to pull, even if valuation debates follow.

The VC Shift to AI: Venture capital firms are aggressively reallocating toward AI-native startups and deprioritizing legacy SaaS bets. The old T2D3 framework aimed to reach $100m in five years through Triple, Triple, Double, Double, Double growth. The AI boom has distorted expectations toward something closer to Q2T3, meaning Quadruple, Quadruple, Triple, Triple, Triple. SaaS companies that cannot meet those targets may struggle to raise additional capital, creating entry points for private equity.

Private Credit

Finally, we are talking about the reason we are all here.

SaaS loans are a unique breed. Because SaaS companies spend aggressively to accelerate top-line growth, their EBITDA is often compressed, which means traditional debt based on 4x–6x EBITDA does not work. Lenders instead found comfort in the same characteristics that attracted private equity: recurring contractual revenue, 80% gross margins, and a thick cushion of sponsor equity.

The rationale was twofold:

If a PE firm buys at 8x ARR and the lender provides 2.5x ARR, enterprise value would need to fall by roughly 70% before the debt is at risk. Given the historical demand for these assets, lenders assumed they would come out whole.

If there is no buyer, the sticky revenue and 80% gross margins allow a company to cut Sales & Marketing and R&D deeply, quickly turning the business into a cash flow machine.

Historically, lenders were even more selective than sponsors. While sponsors focused on NRR, lenders focused on GRR, typically avoiding anything below 85% altogether. At least that was the standard for the lenders I worked with (which admittedly leaves many whose standards I did not know).

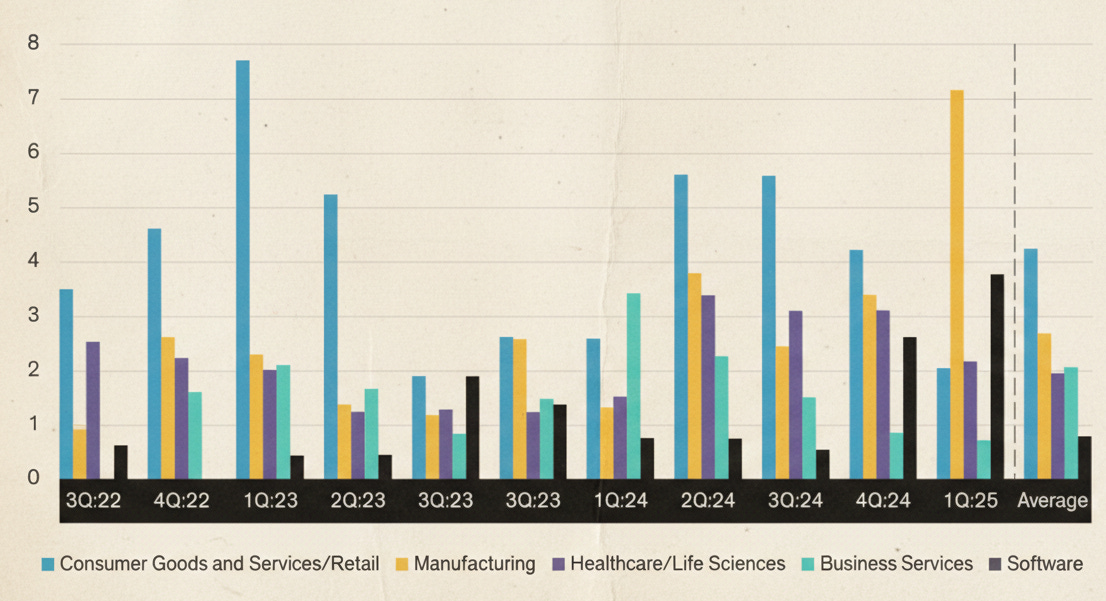

It remains to be seen whether this resilience can withstand real stress. Up until Q4 2024, the software industry had the lowest default rates of any sector. However, as the chart below suggests, that trend broke at the end of 2024 and will likely look even worse this year.

One interesting takeaway from the COVID era is that even when PE firms were paying 16x+ ARR, up from the historical 5x-8x range, lenders did not proportionally increase leverage despite enormous pressure from sponsors and internal originations teams who were losing deals.

Leverage did move from roughly 2.5x to the 3.5x I occasionally saw, but overall lenders were disciplined. Even those higher levels were typically reserved for the best assets or sponsors with long-standing relationships. I am sure they are glad now that they were not “open-minded enough” to materially change their approach. With today’s median EV/NTM multiple sitting at 3.6x, that 3.5x leverage now looks very aggressive.

In my conversations with SaaS lenders, none have seen GRR deteriorating yet, which means there are no mass cancellations to switch to AI. Publicly traded alternatives managers are signaling the same thing. The Blue Owl CEO was even mocked online for saying he only sees green lights. This should not be surprising. AI does not appear to be materially impacting software performance yet. These AI vendors are likely being tested alongside existing software, so companies continue paying for their current subscriptions. Until that changes, which could happen suddenly, and borrower performance starts to decline, the optimistic tone among alternatives managers will persist.

So, what’s next?

Well, even if everyone suddenly realizes that AI will not kill all software companies, the damage is already done. I do not see M&A meaningfully reopening for SaaS, and without PE exits, lenders are stuck. Here is what I think lenders are doing, and will continue doing:

Speaking with sponsors about their plans for portfolio companies (sponsors will surely say everything is fine and the market is overreacting).

Scheduling calls with expert networks like GLG or Third Bridge to check each portfolio company for specific AI risks (like new AI-native competitors).

Using this meltdown as an excuse to demand tighter structures and better pricing on any future credit actions (sponsors will fight back, but they will accept it).

Watching the clock on COVID-era deals maturing in the next two years with their fingers crossed.

One last thing to note. I have been writing that credit markets need M&A to pick up, an accommodating Fed, and the AI boom to continue in order to avoid broader equity disruption. I am still convinced that if the AI bubble pops, it would be terrible for all industries. What I did not fully consider, however, is that if the AI boom continues, it threatens SaaS by putting pressure on the PE firms and private credit funds exposed to software. Most of them have exposure, and often sizable exposure.

This creates a strange dynamic for private credit. The asset class needs AI to sustain broader equity markets while simultaneously hoping it does not disrupt software portfolios. It is a narrow path that requires both outcomes at once. I am not optimistic that this will resolve in the way we would like.

3. Deals on the Block

(click active links for additional details; AND you can now download an Excel file with ALL prior deals)

Lender: GSAM, Blackstone, Apollo

Borrower: Aspen Pharmacare Holdings (APAC operations)

Sponsor: BGH Capital

Facility: $976m (AUD 1.4B)

Pricing: BBSY + 4.75% (BBSY is the Australian benchmark)

Purpose: LBO

Other: 6.5x PF leverage and a covenant-lite deal

Just to be clear: more deals surfaced, but I only flagged ones with details beyond size (pricing, attachment, etc.). If you catch wind of more, send them over - anonymity guaranteed.

4. Bulletin Board

Private Funds Legal Tech x AI event in NYC on February 12th at 5pm ET (free, but RSVP required). LINK

Bloomberg subscription at a 60% discount. It is $149 for a full year versus $399 (LINK). The offer expires on Feb. 16, so you will be seeing this message in my next few letters.

Shortcut.AI, an AI tool for Excel that lets you build models by simply typing requests (similar to ChatGPT). It is free to use up to a certain number of tasks per day (LINK). If you hit your limit before finishing your project, simply upgrade to the Pro plan ($20/month) and enter promo code DEBTSERIOUS (all capital letters) to get 50% off. As a reminder, I don’t personally benefit from either of these offers. I am just saving you money on tools I really like myself.

LoanEdge, a BDC research tool that lets you look into BDC loan compositions, individual loans, which BDCs own a specific loan, and more is kindly providing DEBT SERIOUS readers with a free 3‑month trial (the regular price is ~$3k per year, and it’s higher for institutions). Here is a LINK to the tool. Send an email to Sadaf Khan at sadaf@theloanedge.com and let her know you are from the DEBT SERIOUS community.

Financial Times subscription at 40% discount (LINK). The FT has been pretty disappointing when it comes to covering private credit, often leaning more toward clickbait than the kind of in‑depth reporting you’d expect from a respected newspaper. I also struggle to understand why it costs multiples of Bloomberg…that’s just crazy. Still, if you do end up subscribing, at least take advantage of the 40% discount, which brings the price down to $375 a year… which is still $363 more than I’d personally pay (I’m not a big fan, as you could tell, though the FT Alphaville section is an exception…and it’s free anyway).

That’s the bell — round over. See you in the next.

Aznaur

Aznaur.Midov@KierLior.com

amazing thanks